Data Centers, Dead Mines, and the Moment Copper Stops Playing Nice

In the 1870s, the hills around Morenci, Arizona were not known for mines.

They were known for raids.

Ranchers, including brothers Robert and James Metcalf, rode those canyons hunting Apache raiders and stolen cattle.

They weren’t looking for a fortune. They were looking for payback.

What they found instead were green stains on the rock.

By 1872, those stains turned into the first small digs. By 1881, shafts crisscrossed the hillside. Over time, the hand-dug workings gave way to one enormous open pit.

In the 1960s, that pit grew so large it erased the original town of Morenci from the map.

Today, the Morenci Mine is the biggest copper producer in the United States. It ships more than 400,000 tons of copper a year for Freeport-McMoRan.

The odds are better than zero that some of the copper inside the data center running this very article started life in that pit.

Every AI Data Center Starts With a $60 Million Copper Bill

U.S. data centers pull copper from mines like Morenci for internal wiring, server boards, power lines, and switchgear.

By the time you cost out a modern build, copper accounts for about 6% of total capex.

On a typical 100 MW data center with a $1 billion price tag, it works out to roughly $60 million in copper alone.

That is before you factor in what happens when AI pushes every new build to run hotter, faster, and heavier on the grid.

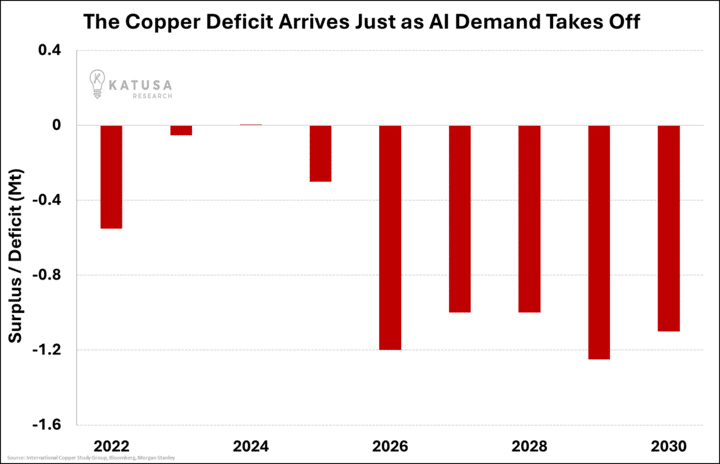

The Big Copper Problem Starting in 2026…

Data centers already chew through a serious slice of the grid.

In 2024, they used roughly 4% of all U.S. electricity. That share could double by 2030 as AI rolls out into everything from search to video to logistics.

Copper sits at the center of that build-out…

Every big facility needs copper-heavy power distribution.

- Cables carry electricity from the substation to the switchgear.

- Busbars move that power across panels.

- Transformers and switchboards rely on copper to stay cool while they push huge currents.

Inside the building, it does not stop.

Servers use copper in their circuit boards and interconnects. Racks talk to each other through copper network cables over short, high-speed runs.

Cooling systems lean on copper heat exchangers to pull heat away from the chips.

AI workloads push all of this higher. More GPUs per rack. More power per square foot. More cooling per watt. New builds are heavier in copper than the last generation.

- Goldman Sachs says AI will drive a 165% increase in data center power demand by 2030.

This means this massive leap will require extensive copper use for both on-site systems and the wider electrical grid.

The numbers add up.

- Copper demand from new data centers alone is running at roughly 400,000 metric tons per year through 2035.

And that’s on top of everything the world already needs for power grids, EVs, construction, and industry.

By the time we hit the second half of this decade, the AI build-out and the existing grid will be fighting for the same metal.

That is the “copper problem” that starts to bite from 2026 onward.

Copper is Critical in the Age of Electricity

The energy system most people see is wires, turbines, and transformers.

The part they never see is the rock.

- To make one tonne of coal, miners move about seven tonnes of material. That sounds like a lot, until you look at copper.

- For copper, you can be moving more than 100 tonnes of rock, water, and other waste for a single tonne of metal.

That gap keeps widening.

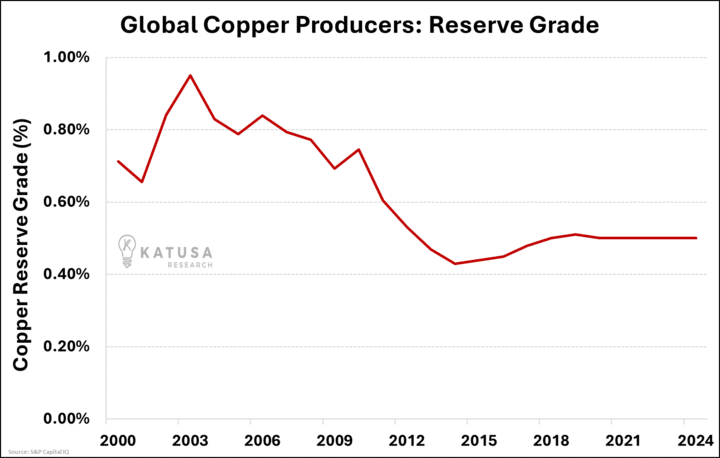

Ore grades at many big copper mines now sit well below 1%. The metal is there, but it is spread thin.

To keep output flat, operators have to dig more rock, process more tonnes, and deal with more residue.

That means higher capital costs, higher operating costs, and a longer slog from first drill hole to first shipment.

Even before AI showed up, the outlook was tight.

Major energy agencies have warned that planned copper projects do not fully cover projected demand for an electrified economy.

The problem is simple: big new mines are expensive, slow to permit, and harder to find. Lead times run to a decade or more.

Few boards want to approve $5-10 billion projects unless they believe high prices will stick.

All of this lands on copper at once.

We are asking the same metal to re-wire power grids, feed electric vehicles, harden data centers, and support

normal construction and industrial use.

At the same time, the easiest deposits are gone, and the new ones are deeper, lower grade, or in tougher jurisdictions.

That is what “copper critical in the age of electricity” really means.

You can watch real supply quietly disappear as high-cost mines shut off, causing price and supply disruptions. Like the world’s second-largest copper mine, Grasberg (in Indonesia), that just shut down due to a major landslide.

The United States is already acting like copper is scarce.

U.S. copper imports hit a record in 2025. As the country talks about reshoring supply chains, it is pulling in more foreign copper than ever to keep up with demand.

In April alone, more than 170,000 tons of refined copper flooded into the U.S., the highest monthly volume on record.

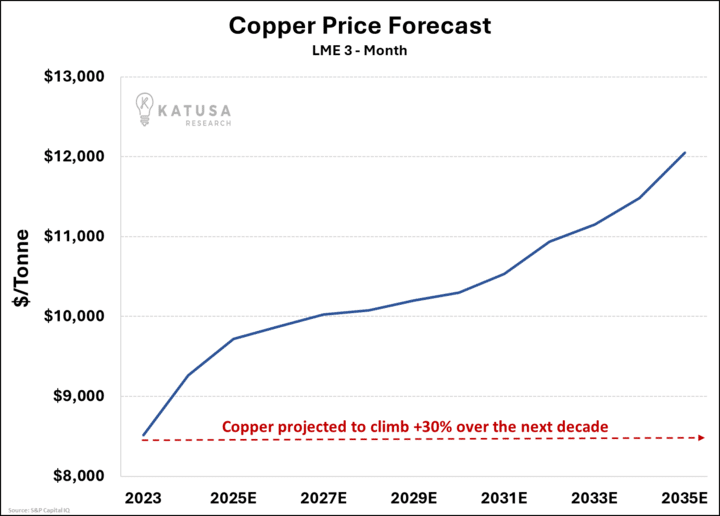

AI, the grid, and EVs are setting up a structural grab for copper.

The physics of mining say supply will struggle, and the long-term forecasts reflect that tightening. Yet the market still prices copper like it is just another cyclical metal.

When a market misreads a structural change, prices usually adjust. For copper, that means prices are likely to rise.

That gap between narrative and price creates the opening for real opportunity.

Regards,

Marin Katusa

P.S. I haven’t stepped foot in this one country since 2008. But the geology is too good to ignore for this one copper stock in our Katusa’s Resource Opportunities portfolio. Get the ticker I am buying when you sign up.