One Water. Half the World’s Food Supply.

Almost half of the world’s nitrogen fertilizer exports pass through ONE narrow waterway.

That sentence should concern you more than oil at $100.

In 1909, Fritz Haber figured out how to pull nitrogen from the air and turn it into ammonia. Carl Bosch scaled it. Together, they built the process that now feeds roughly half the planet.

Today, roughly half the food on Earth depends on synthetic nitrogen fertilizer. Without it, the planet could support about 4 billion people. We have 8 billion.

And right now, the machinery that makes all this possible runs through one of the most volatile regions on the planet.

The Pressure Was Already There

This crisis didn’t start on February 28th. China has been restricting urea and phosphate exports since 2021, with its phosphate ban running through August 2026.

Russia and Belarus remain constrained by sanctions and shipping disruptions despite steady production. Those two pillars weakened first, and the global food system shifted its weight onto the one remaining backstop: the Middle East.

Then Israeli strikes hit Iran’s South Pars gas field, the largest natural gas field on the planet.

The 2025 Iran-Israel escalation temporarily halted roughly 12 million cubic meters per day of gas output.

This time, the damage risks running deeper, and any sustained disruption tightens the global ammonia cost curve immediately.

The Strait That Feeds the World

Oil gets the headlines, but Fertilizer follows the same route, and almost nobody mentions it.

- Countries bordering the Persian Gulf account for ~49% of global urea exports and ~30% of global ammonia exports.

The Strait of Hormuz is also the chokepoint for roughly 44% to 50% of the world’s seaborne sulfur. Which is the key input for producing phosphate fertilizers like DAP and MAP.

Most missed that last point.

QatarEnergy has already halted production at the world’s largest single-site urea facility. Plants across Saudi Arabia and the UAE have curtailed output or gone dark entirely. At least three cargo ships have come under direct attack from Iranian forces since the U.S.-Israeli strikes began.

Reports of sea mines are rising, insurance costs have surged, and vessels are refusing to enter the region.

Markets responded fast.

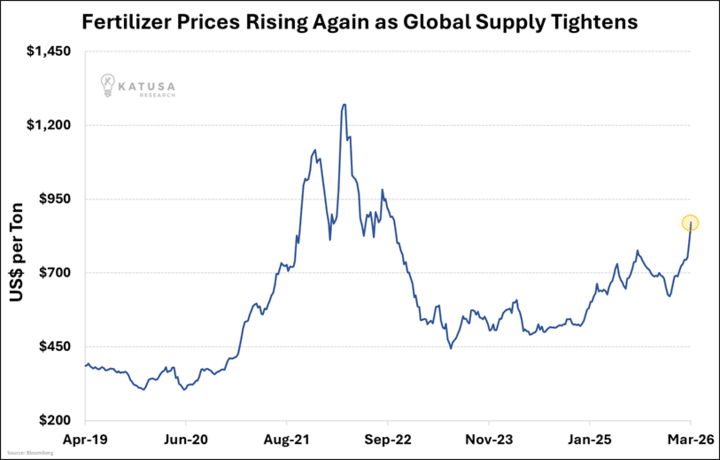

- Urea prices at the New Orleans import hub jumped from roughly $475-$516 per metric ton to $683, a move of 44% in days.

North American fertilizer indexes climbed above $810 per short ton, surpassing last year’s peak.

The fertilizer market doesn’t move slowly when supply chains tighten.

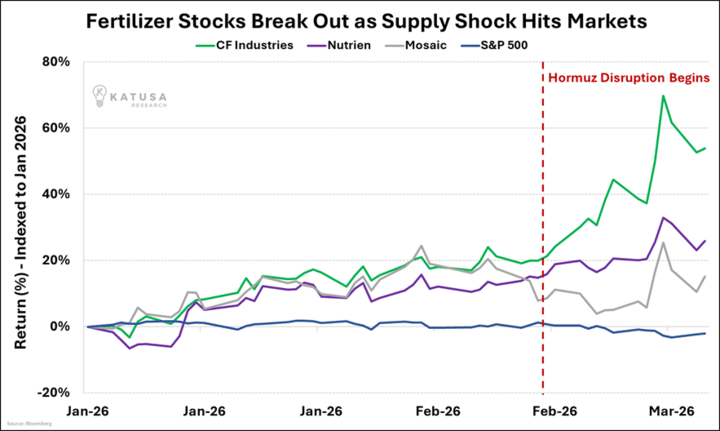

Stocks moved just as fast. CF Industries, Nutrien, and Mosaic have all moved up to multi-month highs since the strikes began.

The equity market priced this before most commodity desks caught up.

The Worst Possible Moment

About 50% of the nitrogen applied to U.S. corn goes in during spring planting.

A vessel loaded in the Persian Gulf today takes 30 days to reach a U.S. port and another three to four weeks to reach interior farm markets.

The American Farm Bureau Federation sent an urgent letter to the White House on March 9th. And their message was direct: fertilizer is stranded in the Middle East during the most critical window of the agricultural calendar.

- Agriculture Secretary Brooke Rollins confirmed publicly that roughly 25% of American farmers have not yet secured their fertilizer for this spring.

The choice facing those farmers is ugly.

They can reduce nitrogen application, switch from corn (which needs heavy nitrogen) to soybeans. Or, absorb the cost and bet on crop prices recovering.

None of those options are good.

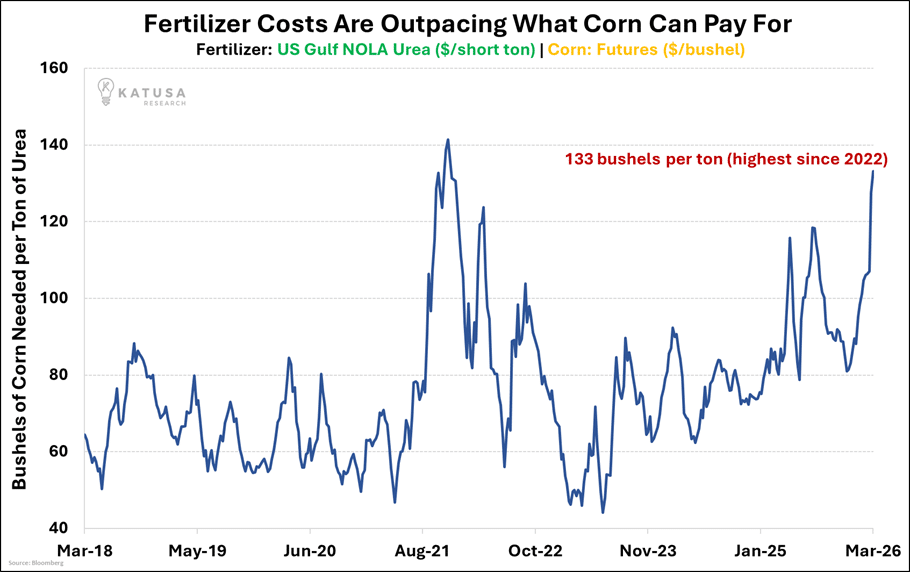

One Iowa corn grower put the math in plain terms. Anhydrous ammonia cost him $492 a ton in 2021. By January 2025, it was $745. Corn prices barely moved. Now add the current shock on top of that.

- At current levels, it takes roughly 133 bushels of corn to buy one ton of urea, the highest ratio since the 2022 spike.

Supply is stranded in the Gulf. And production costs are rising everywhere else.

Washington is Scrambling

Since the February 28th strikes, Dutch natural gas futures have climbed more than 56%. U.S. gas is up roughly 13%. That gap matters because European and Asian fertilizer producers run on expensive feedstock, and they’re getting squeezed from both sides at once.

North American producers running on cheap domestic gas are the only ones whose economics have just improved.

Washington noticed. And the White House confirmed this week it’s pursuing fertilizer from Venezuela and Morocco to offset Middle East disruptions.

The Farm Bureau asked for military escorts through Hormuz, a Jones Act waiver, tariff suspensions, and federal cargo insurance.

Three Pillars and No Backup

Step back and look at the architecture of global fertilizer supply.

-

- China is restricting exports through August 2026.

- Russia and Belarus remain constrained.

- The Middle East now faces direct disruption.

All three pillars took a serious hit within the same cycle.

There is no swing supplier ready to absorb this. There is no strategic fertilizer reserve—unlike oil, nobody has been stockpiling ammonia in underground caverns.

G7 countries don’t maintain fertilizer reserves the way they maintain oil stockpiles. When the system tightens, there is no release valve.

The Lag Is What Kills You

Farmers are adjusting application rates this week and Governments are rerouting supply chains. Buyers are competing for limited volumes at the worst possible point in the agricultural calendar.

But none of that shows up at the grocery store today.

Fertilizer doesn’t inflate food prices at the checkout. It inflates them at the field months before harvest. That lag is what makes this cycle easy to dismiss until it’s too late to act on.

Less fertilizer in the ground today means lower yields at harvest. By the time crop data confirms it, the season is already locked in.

That’s why this matters now—not in Q4.

We profiled CF Industries and several other fertilizer plays in Katusa’s Resource Opportunities in late 2025, well before the Hormuz crisis made headlines.

- CF alone has climbed over 50% since.

KRO subscribers had the playbook before the market priced it in.

If you want to see what we’re watching next, you can join here.

Regards,

Marin Katusa

Get real-time alerts right away. Follow on X: @KatusaResearch and @MarinKatusa

Details and Disclosures

Investing can have large potential rewards, but it can also have large potential risks. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures. Katusa Research makes every best effort in adhering to publishing exemptions and securities laws.

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Katusa Research, and all partners, members, and affiliates harmless in any event or claim.

If you purchase anything through a link in this email, you should assume that we have an affiliate relationship with the company providing the product or service that you purchase, and that we will be paid in some way. We recommend that you do your own independent research before purchasing anything.