In this week’s Investment Insights…

|

Sometimes you have to check back in with a “left for dead” sector.

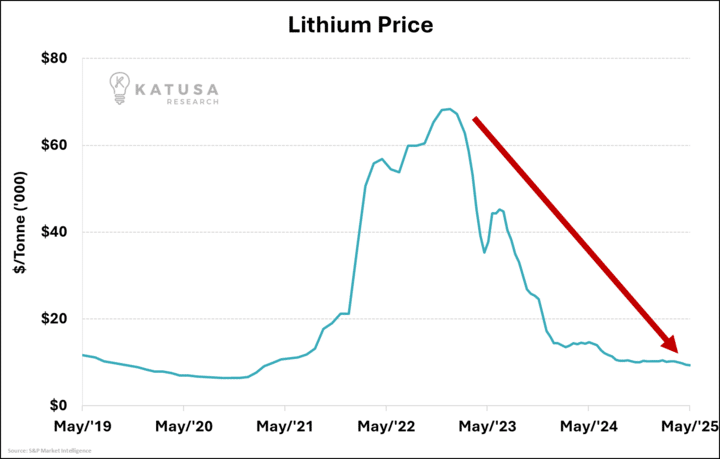

Lithium carbonate prices have cratered more than 80% from their late-2022 peak as wave after wave of new supply hit the docks.

Lithium mines from Australia’s Pilbara region to Zimbabwe pushed global output 35% higher year-on-year — the sharpest surge on record.

According to the IEA, lithium use expanded 30% as EV makers grabbed every cell they could find, but supply growth still outran it.

But prices imploded, taking the producer’s cash flow with them.

The short-cycle nature of hard-rock spodumene meant material came fast; the long-cycle nature of funding and building next-generation mines suddenly froze.

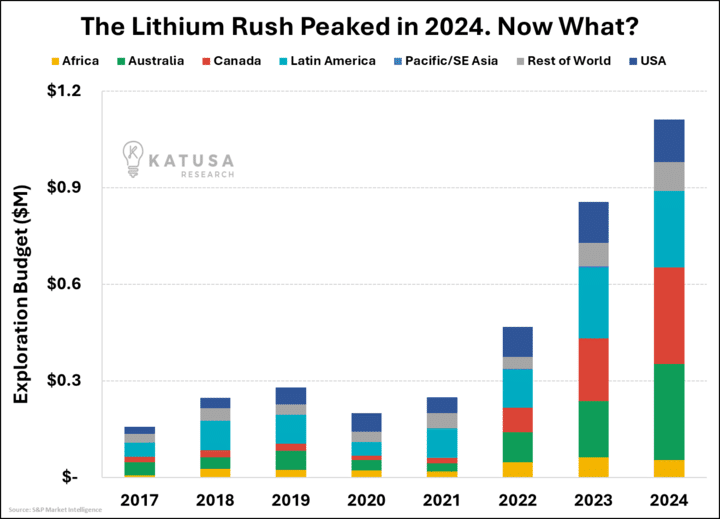

- Global lithium exploration budgets surged to an all-time high of $1.1 billion in 2024, continuing the momentum from 2023’s dramatic increase.

The spending boom reflects sustained investor confidence in lithium demand despite market volatility, with Canada and Australia leading the charge.

That clash — surging need versus overshoot — sets the stage for the metal’s ‘final boss’ test.

If prices can hold this new floor, the bulls may get a clean runway.

Why The Sell-Off Ran Too Far

Cash costs for new lithium from major producers now sit dangerously close to current spot prices.

Even industry giants admit half their projects are now “under”” review”—that’s code for scrapped.

The industry already mothballed several high-cost mines in Western Australia when prices sliced below $10,000 per tonne.

Brine and hard-rock projects can ramp up in 12-24 months, but mega-mines still need 6-8 years.

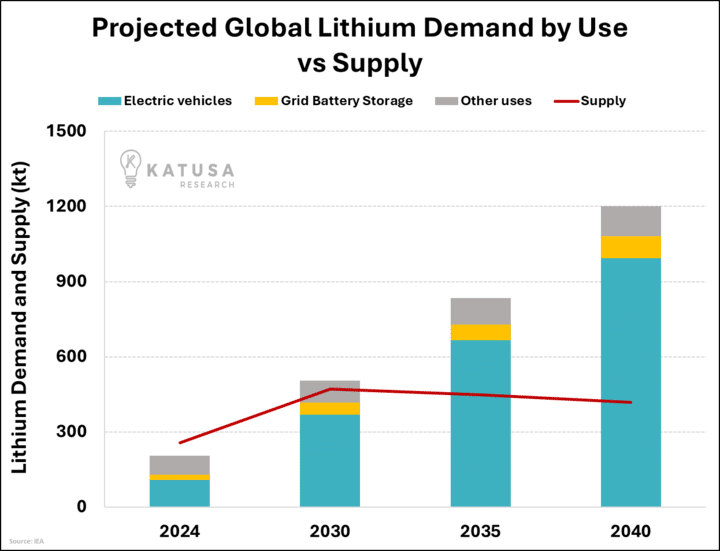

The pipeline beyond 2027 is thin, and the IEA sees a supply deficit opening “by the 2030s” under current policies.

Capital Is Drying Up at the Worst Time

The price collapse wiped out producers’ cash flow just when new projects needed funding the most.

Credit markets that welcomed lithium deals two years ago now slam shut. With capital pipes closing, the forward mine slate thins quickly.

- The IEA calculates that meeting its base-case lithium demand will still require 55 additional average-sized mines by 2035.

Refining bottlenecks are still dangerous: three countries — China, Chile, and Argentina — control roughly 70% of battery-grade lithium chemicals.

Any export curb (think China’s graphite chess move) — or even a paperwork delay — could shove the market from surplus to shortage overnight.

Demand Tailwinds Nobody’s Modeling Right

Here’s the demand catalyst hiding in plain sight: battery storage.

Grid-scale battery projects jumped 85% in 2024 and now consume 15% of all lithium cells.

Catalyst #1: Grid Storage Revolution

Everyone focuses on electric vehicles. They’re missing the bigger story. Grid-scale battery installations jumped 85% in 2024, now consuming 15% of global lithium supply.

Why does this matter? AI data centers need stable power. If small modular reactors slip past 2030 (likely), batteries must fill the gap. That’s pure upside for lithium demand.

Catalyst #2: Chemistry Shifts Don’t Matter

Bears claim LFP batteries will crush lithium demand. They’re wrong. LFP packs use the same amount of lithium per kWh as nickel-rich batteries. The chemical change hurts nickel and cobalt, not lithium.

Catalyst #3: Policy Deadlines Force Action

Watch these dates:

- Late 2025: Chinese subsidies reset, forcing cathode makers to restock.

- July 2026: EU Critical Raw Materials Act kicks in, requiring “friend-sourcing.”

- Ongoing: North American battery plants need a supply to claim $35/kWh tax credits.

Demand isn’t plateauing.

In the IEA’s stated-policies outlook, lithium use has already tripled since 2020 and is on track to triple again by 2035, topping 700,000 tonnes of lithium.

Supply must sprint just to stand still.

4 Signals That Mark What a Bottom Looks Like…

- Project delays: Three Australian spodumene mines already pushed expansion plans; more will follow.

- Take-or-pay offtakes: OEMs locking in multi-year floor prices signal fear that the cheap window is closing.

- Predatory M&A: Strategic buying of assets at a half-built stage, before feasibility ushers in the turn. Rio Tinto bought Arcadium Lithium at fire-sale levels in 2024.

- Exploration Stall: Budgets halted after a four-year boom.

And we’re ticking all four boxes right now.

Finding Plays That Actually Work

Target the cost killers. The cheapest integrated producers will crush competitors when markets turn ugly. These tier-one converters have the muscle to survive price wars and grab market share.

Hunt for permitted brownfields. These sites already spent the big money on infrastructure. When lithium prices spike again, they can ramp up fast while others scramble for permits.

Collect royalty checks. Streaming deals give you cash flow without the headaches of running mines. You get paid whether the operation runs smoothly or hits snags.

What could still go wrong?

Trade wars can kill deals overnight. New tariffs or export bans freeze supply chains and send costs through the roof.

Sodium batteries are lurking but still years away. This tech could put a ceiling on lithium demand, and smart money watches for breakthrough announcements.

Two mega-brine projects in Chile and Argentina could flood markets if they hit nameplate capacity simultaneously. That’s millions of tonnes of new supply in a compressed timeframe.

The Bottom Line

The math is brutal: lithium demand needs to triple again by 2035, but new mine approvals have stalled. Something has to give.

- Supply, meanwhile, must add 55 average-sized new mines just to stay even in the IEA’s conservative scenario.

Track offtake deals and construction slowdowns.

When you see both in the same week, the breakout clock starts—and the first 100-300% gains will come lightning fast.

Regards,

Marin Katusa

Details and Disclosures

Investing can have large potential rewards, but it can also have large potential risks. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures. Katusa Research makes every best effort in adhering to publishing exemptions and securities laws. By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Katusa Research, and all partners, members, and affiliates harmless in any event or claim. If you purchase anything through a link in this email, you should assume that we have an affiliate relationship with the company providing the product or service that you purchase, and that we will be paid in some way. We recommend that you do your own independent research before purchasing anything.