Four years ago, every so-called expert in finance told you the same thing:

America is done.

The dollar will collapse. China owns the future.

I disagreed, and I put that disagreement in writing: a 250-page book called The Rise of America where I laid out the data, made the calls, and signed my name to every one of them.

So how did those calls hold up? Let’s run the tape.

- The S&P 500 sat at 4,200 in May 2021. Today it trades north of 6,800, up over 60%.

- Gold traded at $1,900 an ounce. It now sits above $5,000, a gain of more than 160%.

- Uranium languished near $30 per pound. It punched through $100 in January, more than tripling.

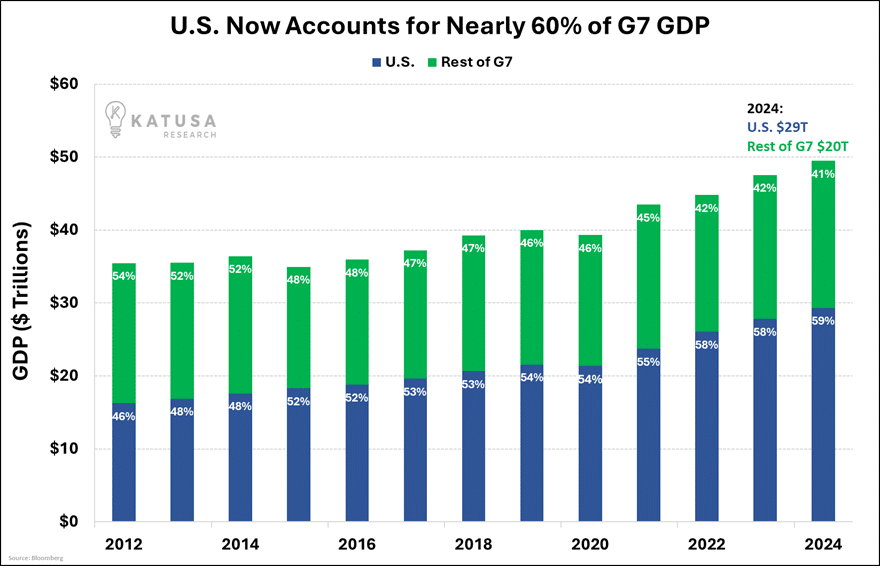

U.S. GDP back then stood at $23 trillion. It has since climbed to $30 trillion and now accounts for more than half the entire G7’s combined output.

When trouble hits, money flows to the USA. The rule of law, markets and innovation ecosystem have no equal. The doomsayers and “America is Finished” crowd got it spectacularly, historically wrong. And the part that matters most to your portfolio…

The best gains from these themes still lie ahead.

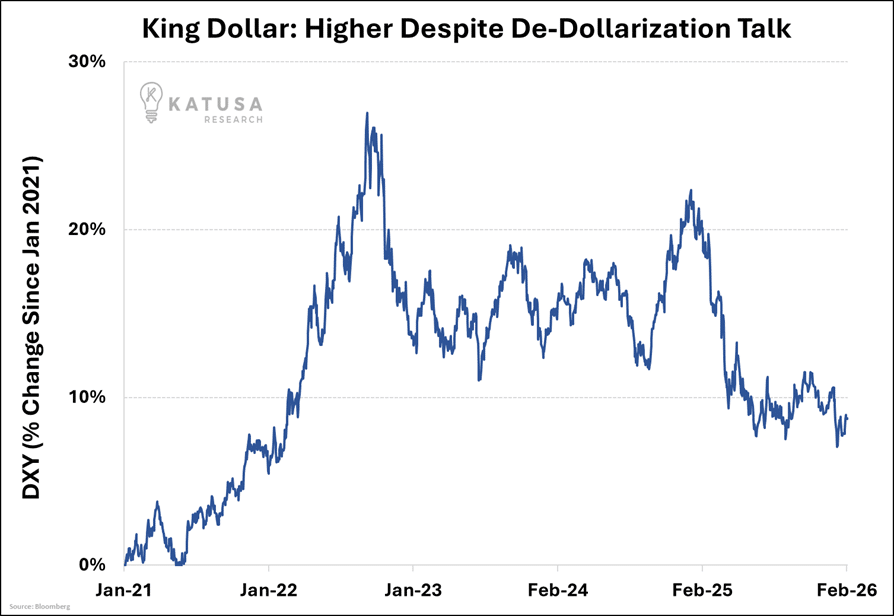

King Dollar, Still on the Throne

In the book, I argued the U.S. dollar would tighten its grip on the global financial system. It held roughly 59% of global reserves then.

It still does.

The Federal Reserve’s SWAP line network functions as a credit lifeline for allied nations, and any country that wants access to dollar liquidity plays by Washington’s rules.

Everyone else gets locked out.

Russia discovered what that looks like in practice.

After the Ukraine invasion, the U.S. froze Russian reserves, severed SWIFT access, and cut Moscow off from the dollar architecture overnight. The BRICS bloc promised a new reserve currency, delivered nothing of substance, and watched the greenback’s share of global reserves barely budge.

China faces its own structural wall.

The renminbi lacks free convertibility, where Beijing’s financial system operates behind layers of opacity.

And China’s property crisis, persistent deflation, and accelerating capital flight have done more to bury the “Chinese century” narrative than any argument I ever put on paper.

America’s Energy Weapon

I argued that energy dominance would hand the United States a strategic advantage no rival could match. Oil, gas, nuclear, renewables: no other country on earth commands that full spectrum.

Every piece of that thesis has landed.

The U.S. now produces more oil and more natural gas than any nation in history.

American LNG shipments replaced Russian pipeline gas across swaths of Europe.

And a wildcard I flagged in 2021, the collision between technology and power demand, blew the door wide open.

AI reshaped far more than Silicon Valley; it redrew the entire energy map.

Every hyperscale data center devours electricity on an industrial scale.

And that surge in demand reignited the nuclear sector, drove uranium back toward $100 per pound, and pushed energy stocks in the S&P 500 up over 20% since January alone.

- The U.S. government just approved 10 new Westinghouse reactor builds and committed $2.7 billion to domestic uranium enrichment.

And on February 12th, the DOE launched its Genesis Mission: 26 AI challenges aimed at cutting new nuclear reactor deployment time in half, speeding grid planning 20-100x faster and building real-time fusion digital twins.

The U.S. government is now explicitly fusing AI with energy infrastructure to power the AI economy itself.

That’s the kind of demand that plays out over decades.

The Resource Supercycle HAS ARRIVED

In The Rise of America, I laid out a collision course.

Electrification, reshoring, and the energy transition would slam into each other and ignite a generational supercycle in critical minerals: copper, uranium, rare earths, and the entire supply chain behind everything from electric vehicles to AI servers.

That collision arrived ahead of schedule.

- The CHIPS Act dragged semiconductor manufacturing back onto American soil.

- The Pentagon now funds domestic rare earth projects to crack China’s stranglehold on processing.

- Copper demand from data centers alone will rival entire nations’ consumption within a few years.

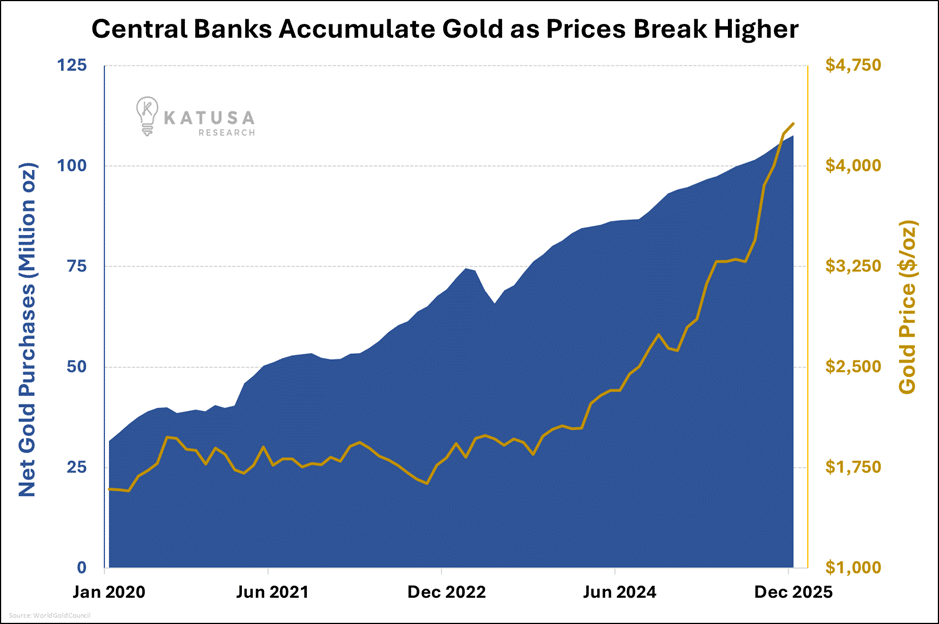

Gold confirms the thesis from a different angle.

Central banks (led by China’s PBOC, now buying for 15 straight months) are stockpiling at a pace unseen in decades.

Gold above $5,000 reflects a market repricing a world where hard assets carry genuine weight again.

The Scoreboard Ahead

The Rise of America holds up better than almost anyone expected.

- Since Q4 2019, the U.S. economy has grown 14.5%, the strongest run in the G7 by a wide margin.

Germany can barely hold above zero, Japan contracted last quarter, and the gap between the U.S. and its peers keeps widening.

Tariff noise, stretched valuations, and political chaos will create volatility.

Volatility shakes out weak hands and rewards those already positioned.

The sectors I identified in 2021 (energy, uranium, gold, critical minerals) remain early in their cycles.

And the structural forces behind them are compounding, not fading.

Central banks are still buying, reactors are still being built. And the AI power buildout has barely broken ground.

If you read The Rise of America, you’ve watched one of the most profitable macro calls of the last five years unfold in real time.

If you haven’t read it yet, grab a copy here.

And if you want the specific stocks, the live analysis, and the portfolio positioning that converts these macro themes into real returns…

That’s what I deliver every month inside Katusa’s Resource Opportunities. You can learn how to join those already in the room right here.

The most expensive mistake in investing hasn’t changed in 250 years.

Never bet against America.

– Marin Katusa

Get real-time alerts right away. Follow on X: @KatusaResearch and @MarinKatusa

Details and Disclosures

Investing can have large potential rewards, but it can also have large potential risks. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures. Katusa Research makes every best effort in adhering to publishing exemptions and securities laws.

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Katusa Research, and all partners, members, and affiliates harmless in any event or claim.

If you purchase anything through a link in this email, you should assume that we have an affiliate relationship with the company providing the product or service that you purchase, and that we will be paid in some way. We recommend that you do your own independent research before purchasing anything.