If you bought silver during the run up to $116 in February, you’ve spent the last six weeks wondering what went wrong.

The metal didn’t break…

The story did.

Because you measured with a yardstick that isn’t built for the job.

The yardstick is the U.S. dollar. The most actively managed asset on the planet, managed for expansion, by design, by people who don’t lose any sleep over your silver position.

I get the appeal. A silver coin in your hand feels more honest than another government promise. You can drop it on a table and hear the argument.

When you measure silver in dollars, you’re measuring a hard asset against a unit that gets actively diluted on purpose.

But there’s a better yardstick. It just doesn’t fit on a bumper sticker.

“Silver Is Money” Is What Trips You Up

You’ve heard the slogan a thousand times. At gold shows, in keynote slides, in the bio of every silver bull on X.

Silver is money.

Maybe you’ve said it yourself. I’ve nodded at it for 25 years out of politeness.

Germany dropped the silver standard in 1871. The U.S. demonetized silver two years later. By 1900 the world ran on gold. Silver’s monetary career is over, the bumper sticker outlived it by 150 years.

The dollar is a managed currency engineered for expansion; silver is a passive lump of metal that gets dug out of the ground. They have nothing in common except that one is used to price the other.

The Era Where Silver Led Every Metal

Step back from the last six weeks and look at the era that matters: the largest M2 expansion in modern history.

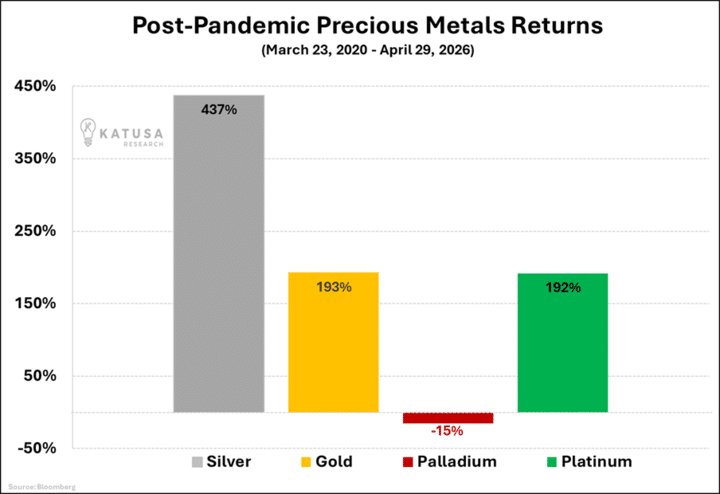

Since March 2020, silver has returned 437% against 193% for gold, 192% for platinum, and a 15% loss for palladium.

That isn’t a coincidence.

Silver does exactly what it’s supposed to do when the unit measuring it gets diluted on purpose. The slogan has been hiding that mechanism behind a worse story for 150 years.

The Yardstick That Actually Works

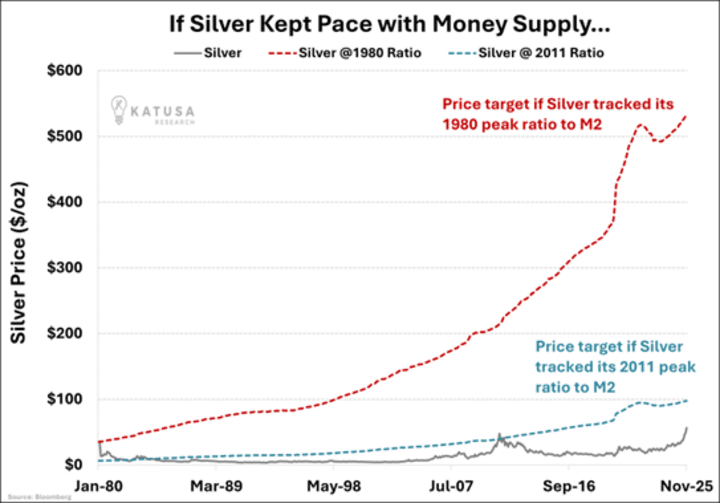

Anchor silver to M2 instead. It’s the broadest practical count of how many dollars are floating around.

When M2 grows, every existing dollar becomes a thinner claim on real things. Silver is real things: in a vault, a panel, a contact, or a circuit.

The price doesn’t go up so much as the unit measuring it shrinks.

Three reference points come out of it.

The 2011 ratio puts silver near $97 today. We hit it in February at $116, then corrected through it.

The 1980 ratio puts silver near $500. Money supply back then was less than a tenth of what it is now. Today’s $70 sits below both.

Treat that as a ruler though, not a target.

I am not calling for $500 silver.

I don’t know anyone who can forecast silver to the dollar without lying to himself first.

The Bumper-Sticker Bulls Just Sold the Bottom

The bumper-sticker bull buys silver because it’s “money.”

When the slogan gets tested by a 30% correction, the thesis breaks with it… sell at the low, buy back at the top. The reason to own silver doesn’t survive contact with a price chart.

The M2 bull buys silver because monetary expansion is structural.

Deficits rarely shrink for long. The Fed’s balance sheet has not gone back to its old world.

And M2 has a habit of growing after every political promise to “get serious.”

That is a different reason to own silver.

But it gives the thesis a spine that survives a bad month on the chart.

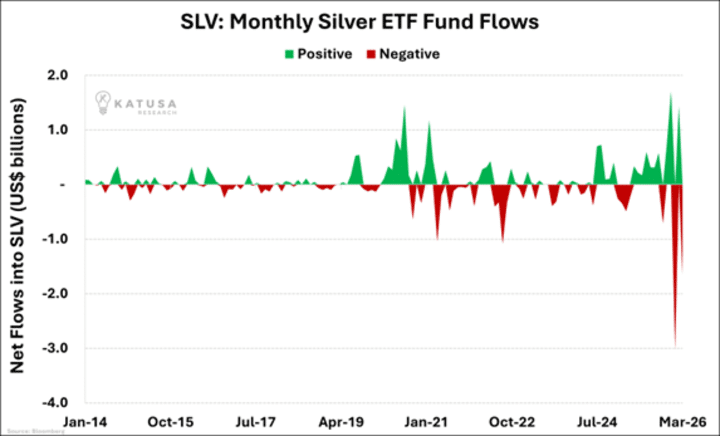

When silver corrected from $116 to $70, the bumper-sticker crowd pulled $4.68 billion out of SLV in Q1 2026 alone.

That’s against just $1.44 billion of inflows.

You Can’t Survive This Trade on a Slogan

Silver investors often get the macro thesis right, then buy whatever has “silver” in the name.

Some of the biggest silver-branded companies do not have the silver exposure investors assume.

Pan American Silver (the company with silver in its name) gets more of its revenue from gold than from silver.

That’s the question the room doesn’t want.

- 74% of the world’s silver comes out of the ground as an accident.

In this month’s edition of Katusa’s Resource Opportunities, we put every major silver producer in the world through the screen.

A few of the things we found:

✓ The most consistent operator in the large-cap group has 5.8 years of reserve life left and management has decided not to fix it.

We name the company and explain why that’s a deliberate choice and not a failure.

✓ The cleanest mid-cap operator in the sector has 2.4 years of reserve life and 100% of its production in a jurisdiction that’s getting harder by the year.

The screen flags it as the strongest operator in the group.

It’s also the riskiest position in the group. Both things are true.

✓ We screened the entire junior silver universe and named the shortlist that meets every criterion we use: geology, balance sheet, and valuation disconnect.

Most of these names trade tight enough that a KRO recommendation would set the price for everyone behind us.

Subscribers see the shortlist.

They get there before the crowd does.

[ Get the April KRO right here → ]

Regards,

Marin Katusa

Get real-time alerts right away. Follow on X: @KatusaResearch and @MarinKatusa

Details and Disclosures

Investing can have large potential rewards, but it can also have large potential risks. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures. Katusa Research makes every best effort in adhering to publishing exemptions and securities laws.

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Katusa Research, and all partners, members, and affiliates harmless in any event or claim.

If you purchase anything through a link in this email, you should assume that we have an affiliate relationship with the company providing the product or service that you purchase, and that we will be paid in some way. We recommend that you do your own independent research before purchasing anything.