On May 12, 2026 the CME Group and Silicon Data announced the first futures contract market in history that settles against the rental price of an Nvidia GPU.

The contracts go live later this year, pending regulatory review.

Terry Duffy, the CEO of the CME, said it directly: “Compute is the new oil of the 21st century.”

It was 1983 when Oil went digital.

And I’ve heard the phrase “this is the new oil” many times over the last two decades.

- But the way I read it, the market is about to start pricing compute the way it already prices oil, power, copper, uranium, and freight.

One week after CME’s announcement, ICE launched its own competing GPU futures product tied to the Ornn Compute Price Index.

Two exchanges racing to financialize the same commodity is how a new market forms.

Back to 1983

On March 30, 1983, NYMEX listed the first WTI crude oil futures contract.

The major oil companies hated it, OPEC hated it.

And for the first eighteen months, volumes were so thin that a lot of people thought the contract would die on the vine.

By 1986, when Saudi Arabia walked away from its swing-producer role and oil collapsed from around thirty dollars to under ten, the NYMEX curve was the only price anyone trusted.

Four years later, Iraq invaded Kuwait and the WTI strip became essential. Every refiner, airline, and treasurer worldwide relied on it to determine future oil costs.

The textbook stops the story there.

- NYMEX made oil prices transparent, hedging took off, and modern energy markets were born.

As a resource investor, the part that got left out matters the most to me.

A producer with a Permian position could finally lock in his selling price years forward, his cost of capital fell, and banks would lend against reserves they wouldn’t touch before.

That’s where Apache, Anadarko, EOG, Pioneer, and Devon came from.

The Contract Industrialized Oil

Halliburton compounded for two decades on the same logic: a forward curve gave their customers long-dated visibility for the first time. And a producer who can see three years out signs three-year service contracts.

Ditto with bankers providing debt based on P1, P2 and P3 resources.

Pipe, rigs, steel, storage, ports: every physical thing upstream of the barrel repriced against the curve.

Financing got cheaper, capital flowed in, long-duration contracts became possible, and the whole upstream supply chain scaled to match.

- The people who made the real money owned the things the contract made valuable.

Spark Spread

Yes, we made up that phrase.

Silicon Data built the index the CME contract will settle against.

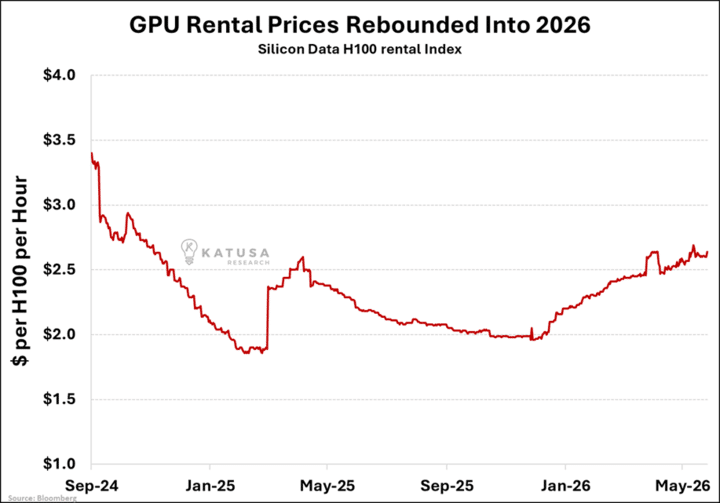

The H100 Rental Index pulls daily pricing from cloud providers, colocation operators, brokered cluster sales, and private rental platforms. It covers more than 80% of the global GPU rental market.

The rate fell through late 2025 as new supply hit the market, then climbed back above $2.60 by May 2026 as premium inventory got scarce.

Picture 10,000-GPU cluster like a Class-A office tower.

The owner carries fixed costs: the power contract, the cooling system, the land lease, the chip financing. Revenue floats with the rental rate.

- At $2.60 per GPU-hour, one H100 running around the clock produces about $22,800 a year in gross rental revenue. The 10,000-unit cluster runs about $228 million a year at that rate.

Move the rate down to $1.90, and that same cluster produces $166 million. That’s the same building, and same costs, creating a $62 million revenue swing, with zero change in operations.

That’s what futures markets get built to solve.

Revenue moves like a commodity while costs sit fixed like real estate, and the gap between them is the operator’s “spark spread”.

CME and Silicon Data are building the instrument to hedge it.

- A GPU-hour also carries something crude oil didn’t: basis risk built into the product itself.

An H100 in a power-constrained region with shared networking and variable uptime is a different asset from one in a secured facility with cheap power, direct fiber, and near-zero downtime.

Early oil futures faced the same problem around crude grades and solved it by pricing quality spreads.

Premium GPU clusters are already trading at a spread to the index.

The best-located, best-powered sites are starting to look less like server farms and more like Permian acreage: scarce, high-margin, and hard to replicate.

The Mirror Trade

At the Milken Institute this month, BlackRock CEO Larry Fink said that compute futures could become a new asset class. Because the U.S. is short on compute, chips, memory, and power.

When a compute carries a public forward curve, governments stop treating AI as software. Instead, it is seen as strategic infrastructure, the same way they treat pipelines, ports, and power grids.

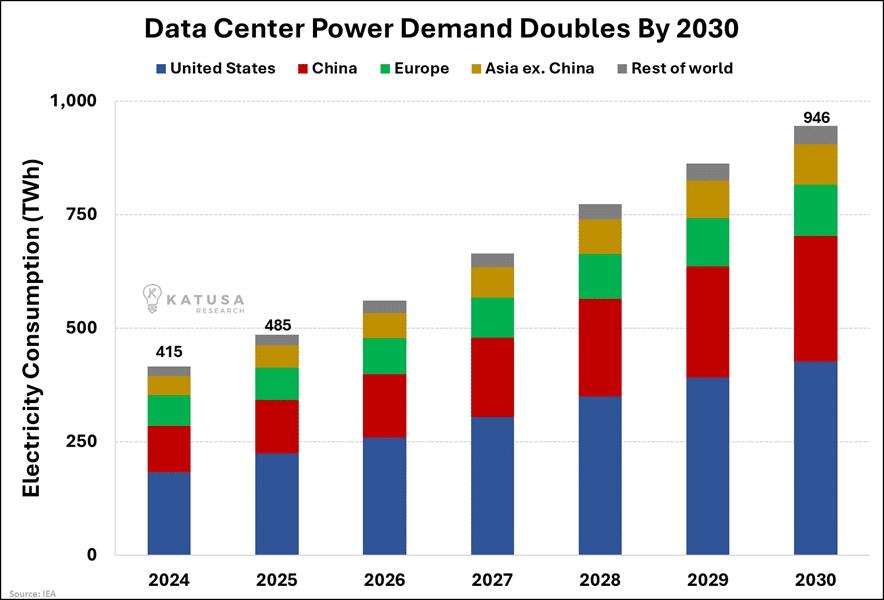

- The IEA puts global data-center electricity at 415 TWh in 2024 and projects it reaching 945 TWh by 2030.

U.S. data centers alone will account for nearly half of U.S. electricity demand growth over the rest of the decade.

The moment the contract goes live, every cluster owner in the world starts treating their power contract, copper supply, uranium offtake, and gas line as a fixed input they’d better lock down.

Before the curve starts pricing in the next squeeze.

This is where Katusa’s Resource Opportunities has an edge.

Everyone is going to chase Nvidia, CoreWeave, and the obvious AI capex names. Those trades are already priced in.

Upstream bottleneck, the physical thing the cluster owner now has to lock down, is where the hidden value is.

Compute behaves more like electricity than copper: hard to store, local, quality-adjusted, full of basis risk, and dependent on bottlenecks the cluster owner doesn’t control.

There are Five Bottleneck Buckets:

- Power. Natural gas, nuclear, SMRs, grid capacity, interconnection queues.

- Metals. Copper, aluminum, silver, rare earths, transformers, switchgear.

- Data-center infrastructure. Cooling, substations, land, permits, transmission.

- Financialization. CME futures, forward curves, compute hedging, structured products.

- Scarcity signals. GPU rental rates as a live market read on AI infrastructure stress.

Reuters reported this week that U.S. power consumption is on track to hit new records in 2026 and 2027, with most of the growth coming from AI data centers and crypto.

Compute futures are the new price signal to watch.

And power, uranium, gas, copper, transformers, and grid infrastructure are the physical bottleneck on the other side of it.

The mirror trade is on the bottleneck side.

Regards,

Marin Katusa

Get real-time alerts right away. Follow on X: @KatusaResearch and @MarinKatusa

Details and Disclosures

Investing can have large potential rewards, but it can also have large potential risks. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures. Katusa Research makes every best effort in adhering to publishing exemptions and securities laws.

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Katusa Research, and all partners, members, and affiliates harmless in any event or claim.

If you purchase anything through a link in this email, you should assume that we have an affiliate relationship with the company providing the product or service that you purchase, and that we will be paid in some way. We recommend that you do your own independent research before purchasing anything.