Dear Reader,

It’s not a secret…

In just 19 months, lithium has plummeted by more than 85%.

Mines are shutting down. Investor cash is drying up. And the market still can’t seem to find a bottom.

But for a select few lithium companies and their investors, this is the best news ever…

For one, Australian-based mining giant Pilbara Minerals just acquired Lithium small cap Latin Resources for $370M, and shares soared over 50% on the news.

And second, because this is a real blood-in-the-streets moment for lithium and the companies that mine it. Which means it’s time, as Buffett said, to be greedy when others are fearful.

In the case of lithium, that’s especially great advice.

Because the current fear in the lithium market is based on three bald-faced lies.

And determining what’s actually true could be the fast-track to a fortune.

According to the big banks, the collapse of lithium has been caused by several factors, such as falling EV sales, a shift towards less lithium-hungry hybrid EVs, and mine over-production.

Only, none of those matches up well with reality.

The Death of EVs Is Greatly Exaggerated

Supposedly, the falling demand for lithium stems from a reduction in EV subsidies and a slowdown in mainland China’s EV sales.

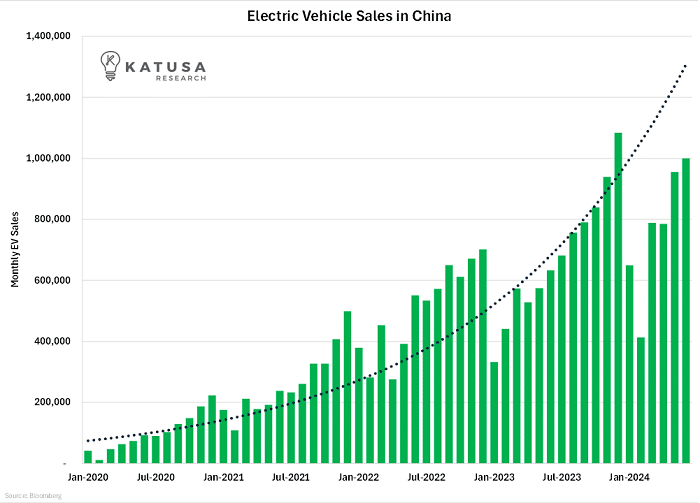

- Fact check: Chinese EV sales are stronger than ever, with 2024 being the best year yet by far. For example, in 2024 EV sales represented 41.9% of all vehicle sales in China.

The chart below shows the monthly EV sales in China.

EV demand has also continued to rise around the world. In 2023, sales volume increased by 35%.

One of the only places short-term EV demand forecasts have shrunk is the U.S.: because it won’t be able to produce enough.

Analysts are slowly catching on to the truth that the EV market never slowed:

“The reports say underlying demand for electric vehicles has disappointed, but to us, it still looks to be very strong.” – Auscap

Media reporting that EV adoption is in reverse is not evident…

– 2024 J.D. Power report

In a November 2023 lithium report, S&P actually raised its EV forecasts through 2027.

There’s another hidden reason provided for the alleged lithium demand drop, though: the hybrid EV (PHEV) vs. battery EV (BEV) war. Due to their smaller batteries, hybrids require less lithium than battery-powered EVs.

And last year, for the first time since 2020, plug in hybrid sales grew faster than battery car sales.

But that’s already quickly reversing. PHEVs are simply bridge cars—lower-cost EVs that help consumers overcome range anxiety and wait until charging infrastructure is built out.

In China, PHEVs rose from 18% market share in 2021 to 30% in 2023. But the trend is already over, with predictions that they will decline from 2025 on.

And in the U.S., Battery EVs have already soundly won.

They will be 81% of the market this year… 85% in 2025… and 93% by 2029.

In other words, the EV market is quickly becoming far more lithium-intense.

The longer miners believe that EV sales are slowing and that new EVs will use less lithium, the worse the industry will be prepared to provide adequate supply.

And to make things even worse… the supposed “over-production” of lithium is in an extremely precarious position—and much of it has already shut down completely.

Last Mine Standing

The rapid rise in lithium prices—1,380% from Nov. 2020 to Nov. 2022—warped the market, causing a surge in production that cannot and will not last. (Note: You can follow Lithium Prices here)

- Africa, for example, saw a rise in “artisanal mining.”

It’s estimated that two-thirds of African lithium supply in 2023 was mined by hand—and that’s almost exactly the global market surplus in 2023.

But mining by hand is price sensitive. It certainly cannot be sustained under an 85% drop in lithium prices. At current prices, much of the “marginal” or high-cost production is almost certainly losing money every day they operate.

High lithium prices also encouraged low-grade spodumene and lepidolite producers to begin mining—and many have already stopped.

In January 2024, Core Lithium completely halted mining at its operation in Australia.

In March, Arcadium Lithium announced that it will reduce lithium output.

Morgan Stanley anticipated production at Greenbushes, the largest hard-rock lithium mine in the world and a low-cost producer, to push the globe into long-term oversupply.

But instead of ramping up production, Greenbushes announced they were cutting lithium production in mid-2024.

And in China, two major lithium units were taken offline in July 2024 and we suspect many others are on the verge of unprofitability.

Altogether, double-digit lithium mining capacity has already been removed, more than the 2023 surplus.

And high-cost and pureplay lithium producers continue to exit the market, postpone projects, and slash investment.

But remember: Demand hasn’t gone anywhere.

This is great news for a few disciplined miners and developers with enough cash on hand to play the long game.

They’re pouring cash in while there’s still blood in the streets.

Even Warren Buffett announced his own lithium project in mid-2024—when lithium was at its lowest.

While lithium won’t necessarily skyrocket again any time soon, it should recover to an above-historical level.

And when it does, miners and developers that make it to the other side with low-cost production are likely to be sitting on gold mines.

The Katusa Research Special Situations Team has identified a special company…

Sitting on a massive, low-production-cost lithium asset in a great jurisdiction.

They’re doing the hard legwork now while the price is low and competition is capital-deprived.

As you saw in the news, Australian Mining giant Pilbara just made the first big $500M splash in the market.

Lithium blood is in the streets…

Are you prepared?

Regards,

Marin Katusa and the KR Special Situations Team

Details and Disclosures

Investing can have large potential rewards, but it can also have large potential risks. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures. Katusa Research makes every best effort in adhering to publishing exemptions and securities laws. By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Katusa Research, and all partners, members, and affiliates harmless in any event or claim. If you purchase anything through a link in this email, you should assume that we have an affiliate relationship with the company providing the product or service that you purchase, and that we will be paid in some way. We recommend that you do your own independent research before purchasing anything.