I bet you can’t name the company that built the world’s first rechargeable lithium battery.

If you said Tesla, Panasonic, or any name with “battery” in it… you’re off by fifty years and an entire industry.

The patent is US 4,009,052 and it was filed April 5, 1976. The assignee of the patent was Exxon Research and Engineering Co.

The oil company invented the battery.

And then they walked away from it.

In October 1973, OPEC cut supply and America felt its first energy chokehold. You’ve seen the photos of gas stations rationed by license plate with lines around the block.

Exxon wasn’t surprised.

Their own geologists had quietly concluded years earlier that global oil would peak by 2000. And the embargo was the public confirmation of a private thesis.

The battery was the hedge against the day their main product ran out. Then oil prices recovered, peak-oil got pushed out, and Exxon shelved it.

Fifteen years later, Sony commercialized a version. Exxon spent the next four decades pumping crude oil.

- Last month, 50 years after Whittingham filed that patent, ExxonMobil produced its first battery-grade lithium from an Arkansas brine field.

The same company that invented the battery, abandoned it, and returned to mine the metal behind it.

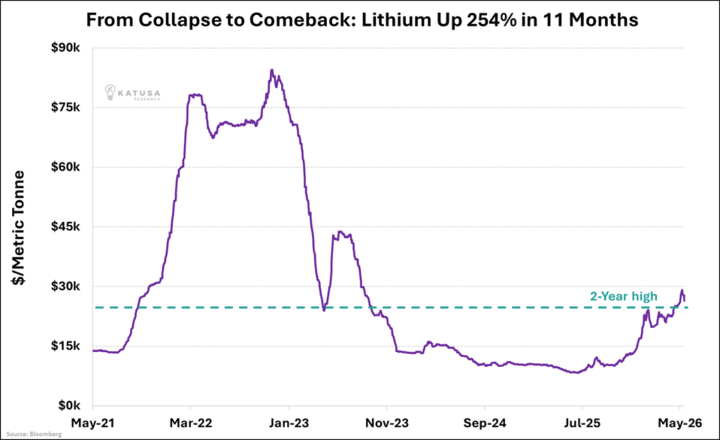

And “white gold” just hit a two-year high.

Below Cash Cost Was Always Temporary

To see why, rewind eleven months.

In June 2025, lithium fell to $8,259 per tonne, below what it costs most miners to pull it out of the ground.

Projects went dark and technical teams scattered. Feasibility studies dropped from dozens per year to fewer than ten, and new exploration dried up with them.

The metal powering the grid buildout was selling at a loss.

Miners need 6 months of sustained high prices before they commit to a restart. And at least twelve more months from that decision before the first production comes out the other end.

The industry spent two years digging a supply hole, it will take three years to climb out of.

Heading into 2026, S&P Global’s base case called for lithium to remain in a 109,000-tonne surplus. Smaller than 2025, but still a surplus.

The market wasn’t priced for a supply shock. Then two came back-to-back:

- On February 25th, Zimbabwe’s Minister of Mines suspended all lithium concentrate exports with no warning and no end date.

Zimbabwe was on track to produce 124,000 tonnes LCE in 2026, more than the entire S&P-projected global surplus and supplied 15% of all spodumene shipped into China.

A partial lifting came April 27th, but a 10% export tax remains, and a full concentrate ban is locked in for January 1, 2027.

- CATL’s Jianxiawo mine, the largest hard rock lithium operation in the world, remained offline after restart delays that began in late 2024.

Zimbabwe’s disruption alone was enough to wipe out the entire forecasted cushion. Add CATL’s offline output, and the surplus S&P projected for 2026 had turned into a deficit before Q1 was over.

Rack up the Lithium

The Iran war put 20% of global oil and LNG flows through the Strait of Hormuz under threat, pulling forward EV buying by years.

The UK recorded 86,120 EV sales in March 2026. EU battery electric registrations rose 51% year-on-year, with more than 500,000 units sold across Europe in Q1.

BYD pushed a record 135,098 vehicles overseas in April.

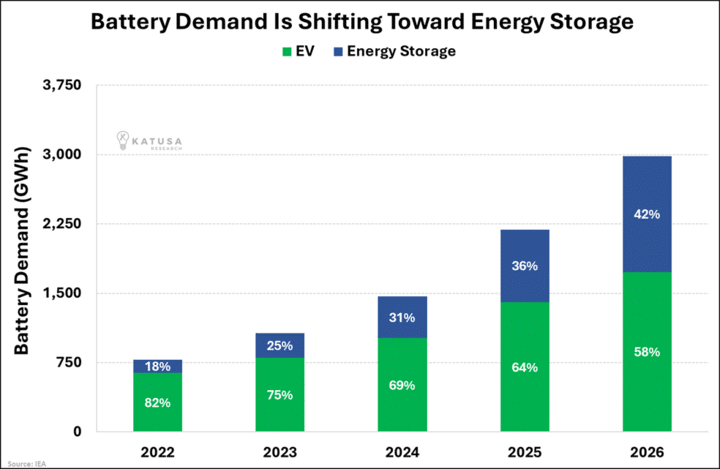

The fastest-growing source of lithium demand is no longer cars.

BNEF surveyed 22 of the biggest battery makers.

- They found that energy storage will make up 42% of battery cell production by the end of 2026. This is a rise from under 20% in 2022.

At least 11 cell plants built by companies like General Motors, Ford, and Volkswagen switched from making EVs to storage devices because grid demand for lithium is outpacing car sales.

EV sales are no longer the binding driver of lithium, storage is.

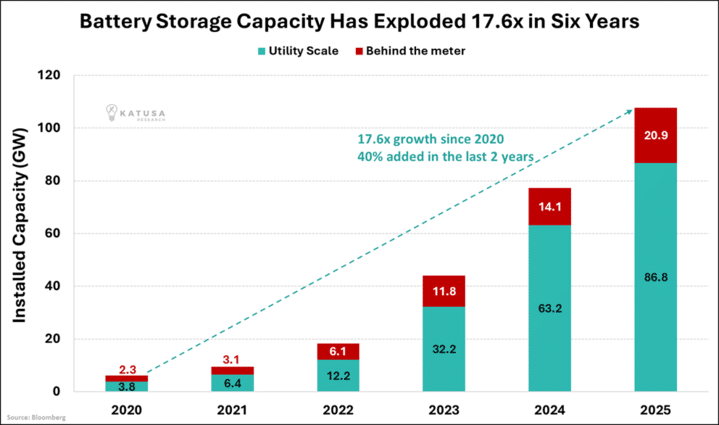

Battery storage’s installed capacity has increased almost 18x in 2025 compared to what it was in 2020.

40% of that growth came in the last 2 years.

The driver behind the steepest part of that curve is AI.

A hyperscale data center burns 100+ megawatts continuously, and the grid can’t ramp that fast, so the data center brings its own battery.

Every rack going online is a lithium order, indirectly. That’s a demand vector that didn’t exist in any 2023 forecast.

3 Lithium Engines Running

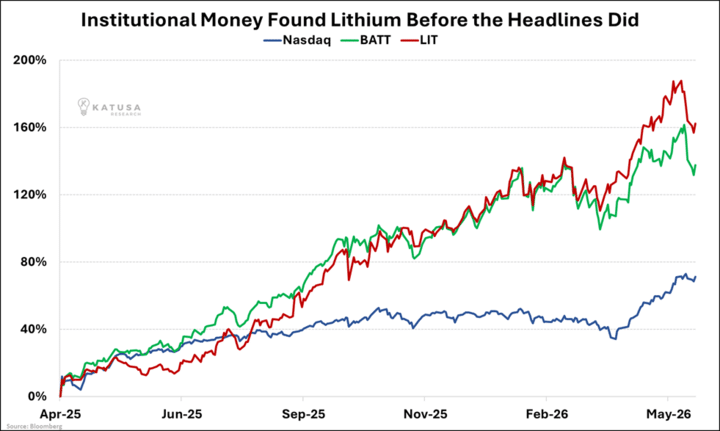

The market’s already moving…

LIT, the Global X Lithium and Battery Tech ETF, returned 162% over the past year.

BATT, the Amplify Lithium and Battery Technology ETF, returned 138% over the same period. And that’s against the Nasdaq-100’s 71% gain.

The US government moved too…

The DOE loaned $2.26 billion in Thacker Pass, Nevada, and the USGS found large lithium deposits in the Appalachian Mountains, enough to cover 328 years of US imports.

The reason: China still supplies over 70% of the lithium-ion batteries the U.S. imports.

The last comparable setup was 2016, when lithium ran on a confirmed supply shortage with EV penetration under 1% of new car sales.

The last time this setup, lithium tripled. And that was with one demand engine.

There are three running now:

EVs, grid storage, and AI infrastructure, with the surplus S&P forecast for 2026 already gone.

Exxon’s bet in 1976 was that oil would eventually run out. They were right about the depletion thesis, just fifty years too early.

They reopened the bet last month.

Fifty years later, the world is building that storage faster than any supply model projected two years ago.

Read the full breakdown of fast-moving commodity sectors inside Katusa’s Resource Opportunities.

Regards,

Marin Katusa

Get real-time alerts right away. Follow on X: @KatusaResearch and @MarinKatusa

Details and Disclosures

Investing can have large potential rewards, but it can also have large potential risks. You must be aware of the risks and be willing to accept them in order to invest in financial instruments, including stocks, options, and futures. Katusa Research makes every best effort in adhering to publishing exemptions and securities laws.

By reading this, you agree to all of the following: You understand this to be an expression of opinions and NOT professional advice. You are solely responsible for the use of any content and hold Katusa Research, and all partners, members, and affiliates harmless in any event or claim.

If you purchase anything through a link in this email, you should assume that we have an affiliate relationship with the company providing the product or service that you purchase, and that we will be paid in some way. We recommend that you do your own independent research before purchasing anything.