Special Note: On June 6th, 2018 at 1:30pm PDT (4:30pm EDT) Marin Katusa will publish the specification on his “The Next Pebble” bet in the June issue of Katusa’s Resource Opportunities.

Are you a Speculator or Investor?

If you relate with the Greasers in the book The Outsiders by S.E. Hilton you are a speculator. If you relate with the Soc, you’re an investor.

Just kidding.

I’ll get back to the novel Outsiders in a minute…

I’m known as one of the largest financiers in the junior resource sector. If there is a Private Placement being pitched, I’ve most likely seen it.

Because of this, I am regarded as a speculator. These juniors are speculations because most don’t have any cash flow or profits.

In fact, most people who don’t subscribe to my newsletter would call me a speculator.

But those who follow my work know better.

Here’s a little about me…

Other than an amazing family that would support me on any venture during my formative years (the greatest blessing one can have) – I had nothing tangible to my name.

No money.

No connections in the stock market.

I didn’t even know anyone who worked for a publicly traded company (now you could see why I related with the greasers).

But I wanted to learn. So, I started where every nerd would start – the library.

I read pretty much every book on investing I could get my hands on.

I read hundreds of books on subjects ranging from value investing to speculating. From the CFA program to get rich guru nonsense, I absorbed it all.

My background is mathematics, and the reality of my predicament was that the mathematics proved I needed to “work it” with the little capital I had access to.

I also knew the teacher’s salary I was on (I started out as a High School Math teacher) wasn’t going to provide me with the float to become a mini Warren Buffett.

Not to get distracted, but I believe the whole educational system fails our students on many fronts. But none more so than the lack of education on finance and, specifically, how to make money.

Let me explain…

Teachers at the school where I taught were encouraged to get involved in extracurricular activities for the students. Rather than being a basketball or volleyball coach (which I had zero interest in doing), I made a proposal to the principal: I asked to create a finance club for any and all students.

It was frowned upon by the administration and most of the faculty. Yes, many of the teachers looked at me like I was an alien, and that wanting money was inherently bad. Crazy!

Good thing a consistent trait throughout my life has been not giving two ****s about what others think (maybe it’s the East Side in me, or the fighting Slavic spirit, I don’t know). I personally found it ridiculous that teachers were lauded for leading walking clubs, poetry clubs, and knitting clubs. And yet I was looked down upon for creating the finance club and encouraging students to want to be financially well off.

Rather than taking the kids to a basketball tournament on the school bus, I took my “team” on the school bus to a private tour of a public company’s facility. We also had a president pitch his company to us. And we attended an AGM.

I tried to be a role model to these kids because I taught math differently than most teachers. By making math about money, I tried to make math cool. To some degree, I believe I succeeded.

Today, the students who were members of my finance club are doing fantastic.

One is a mining engineer executive at one of the world’s largest mining companies. Another is a fund manager. Another is a bank manager. Two run their own businesses. And every one of these students had a learning disability. Is it a coincidence that of the 6 students who were in my finance club for two years, 5 are directly working in business and finance?

There is no doubt I started as a speculator.

And almost 20 years in, I can say that a successful speculator evolves into a hybrid between a speculator and an investor.

But you can’t be both a Greaser and Soc… can you?

Let me explain the Journey of a Speculator.

Financial literacy is a must.

As is technical understanding of the industry you are analyzing.

If you do not have both, you are a gambler.

But how do you reconcile the two – how do you become both a Greaser and a Soc? Cherry Valance (the female lead character) had it all figured out in The Outsiders – can’t the two sides just get along?

Stick around, because you are going to learn something valuable in this missive.

Remember These Four Letters

F-C-F-P.

No, FCFP is not F***OFF in Russian.

In 2014 when I bought my first large block in Ross Beatty’s Alterra Power, I bought it not because I liked Ross (I do, but not that much!), but because I liked the potential upside and what I believed was hidden financial value in the company. The financials were complicated, hence the financial literacy portion of my comment above.

I wasn’t a wind power expert, nor was I a run of river expert. But I learned what I could, visited as many sites as I could and I used the best consultants in the industry for questions I couldn’t answer myself.

I walked many of the well-known analysts through financial details on Alterra. And I even corrected a major financial data source that the industry uses for their inaccuracy on how the debt was being reported (you’re welcome).

But what really stood out for me was that my calculations showed me Alterra was going to be generating more cash than it was burning. And I believed the company would start spitting out a dividend.

Over the next 36 months, I bought millions of shares to become one of the largest shareholders. Again, not because I wanted to support Ross or because I liked him, but rather because this was a compelling investment opportunity.

The fact that Ross was the largest shareholder and Chairman of the company made the experience that much more enjoyable because there is nothing better than working with people you like. And that’s a key statement. I really do like Ross and have an incredible amount of respect for him. And if the exact financial proposition was present but the management team wasn’t one I respected, or liked, I would not have bothered. Stay away from bad people.

Was my big bet on Alterra a speculation or an investment?

The answer: It was a hybrid of both.

The costs of green energy had dropped significantly over the last decade. And I believed they would continue to do so (speculation). I believed that the day would come when green energy would be economic without government subsidies (speculation, and one that got the most pushback from gold bugs).

I also believed that cost of capital would remain low during the investment horizon (speculation).

The complex financial models I created to determine the NPV of the producing assets weren’t speculation but rather based on financial investment models. Though some of the key inputs, such as future power rates, were speculation.

After following Ross’ own evolution in the green energy space (he got into geothermal in 2008—and I visited their first operation in 2008), it wasn’t until late 2014 that Ross and I met privately at his favorite coffee shop in Vancouver where I laid out my thesis for Alterra. It was a delicate combination of both speculative assumptions and investment fundamentals.

We went through my 20 plus pages of math and Ross replied, “You’re a nerd”.

I responded with, “A cool nerd”.

My evolution to a hybrid of speculator meets investor began.

Kind of like a perfect mix of Greaser and Soc. Cherry would be so proud.

I believe that in order to obtain success in the current cyclical resource markets, any investor must be a sound speculator and any speculator must be a sound investor. Elements of both are required in every investment decision in the equities market.

For example, whether you are a Soc or a Greaser running the FCFP on Alterra, you have to make multiple assumptions for the inputs in your financial models.

And this goes for any complex investment model for any company in any sector.

For all the Soc (investors) out there who look down on the Greasers (speculators), sorry to pop your bubble. When you create your own FCFP model, you may take a consensus of analysts’ assumptions to get your numbers, but all you are really doing is taking the consensus of a bunch of Greasers. You might as well understand what it takes to be a Greaser in order to be able to come up with your own sound speculative inputs.

It is shocking to me how many complex financial models I come across from the “big bank analysts” that use absurd input values based on a consensus of 12 analysts.

Really?

How about you come up with your own inputs and take responsibility and not blame the “consensus”?

Anyways, I think you get my point.

Dividends May Not Sound Sexy, but Making Money Is

Alterra was an excellent example of using a hybrid approach of being a speculator and an investor. Because part of my investment thesis was this: What is the true NAV (Net Asset Value) of the company such that a larger company would buy out Alterra?

Again, I published my data for over 12 months, and it was a mix of speculation and investment prowess.

Was it easy? Hell no.

Did I doubt myself at times? Yes.

When I was underwater on my first and second and third tranches, did I re-assess my models and inputs—yes! That’s the point of having skin in the game—I care.

Would an analyst who has no skin in the game care as much? No. It’s not possible. I had millions into the deal and you better believe I kept a keen eye on the company at all times.

How could an analyst who isn’t allowed to own the stock care as much? It’s just not likely.

A global recession can drop the price of coal from over $300/t to $100/t and cause the dividend paying coal stock you bought at $40 to cut its dividend, resulting in the stock dropping to $10 overnight. Similar situations have played out countless times.

In your investment model, what assumptions (speculation) did you make on the price of the commodity?

I often get asked about dividends in my models…

And I’ll share some analysis with you today, for both the Greasers and Socs out there—because as they will find out, both have it tough in these markets…

There are many factors that can impact the performance of a company’s dividend. Not all dividend yields are equal.

I’ll break down some of these factors in more depth below.

Very few mining and energy companies have the Warren Buffett “moat” around their businesses. But when you come across one (and they are out there), it takes both speculation and investing techniques to succeed.

Step 1 – Understand Debt and Debt Free

One of the most important indicators I look at for dividend stocks is the amount of outstanding debt on the balance sheet.

Debt in a cyclical resource market is very dangerous.

If two companies offer the same dividend yield – but one has no debt load and the other a debt facility that they need to service – how do you proceed with your analysis?

Start with the payout ratio.

A company’s debt can impact many things. But one key indicator we look for at Katusa Research is how closely a company’s debt is tied to its payout ratio.

A payout ratio is the ratio of the amount of money the company paid out in dividends, divided by the company’s net earnings.

Step 2 – Payout Ratios

A payout ratio below 30% generally means that the company is reinvesting profit back into the company and continuing to grow its operations more so than it is paying back shareholders. It also demonstrates strong economics if the dividend is above industry peers. Following up on the ROI of those management decisions is critical in assessing if management is doing the right thing with this payout ratio.

Knowing the company’s margin compared to its peers within the same industry is crucial. Understanding the history of the dividend is also critical. Is the dividend relatively new, or is it increasing year over year, or decreasing?

A payout ratio between 30-55% is generally considered healthy, as the company is splitting its focus between giving back to its shareholders, while still retaining some of its cash to grow the company with.

A payout ratio between 55-100% may look good for the investors on paper. But when the ratio is this high it could mean that either the company has no growth plans or that their dividends are unsustainable. Make sure you understand the company’s debt servicing requirements if the commodity price drops.

Payout ratios higher than 100% or lower than 0% can exist as well. These tend to be short-term occurrences due to special dividends and extraordinary circumstances. A company that is paying out more in dividends than it makes, or is paying out dividends when it isn’t making any money, is not going to stay in business for very long. I’ve seen it in the oil patch.

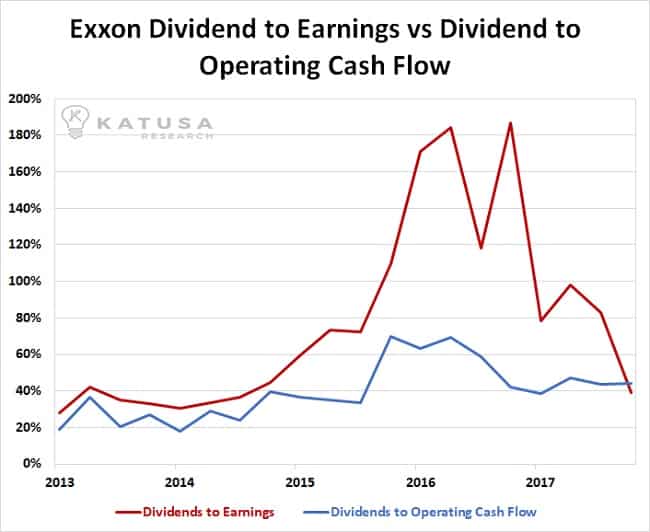

Casey Study: Exxon Mobil

Let’s take a look at the longest dividend paying oil company in the world, Exxon Mobil (XOM:NYSE) over the last five years:

At the beginning of this period, Exxon had low debt, strong income, and a very healthy dividend payout ratio of 28% for what is historically a low margin business that requires significant reinvestment to maintain production or grow conservatively.

However, as oil prices started their downturn towards the end of 2014, Exxon’s profits followed shortly (hitting their lows in 2016).

During this time, Exxon was committed to maintaining its dividend. But to do so, it was sacrificing its balance sheet. What followed is that its debt load skyrocketed, along with its payout ratio.

Of course, 2016 was a very difficult time for all oil companies, let alone Exxon Mobil. But if you were only looking at Exxon’s dividend yield during the period it would have been hard to tell.

Why?

Because Exxon maintained a steady dividend through the entire length of the downturn.

Without looking at the dividend payout ratio as well, investors would only have seen one side of the story – a steady dividend. On the other side, Exxon’s debt load more than tripled while its market value shrank by nearly one-third.

Limitations of the Payout Ratio

With that said, the straight payout ratio is not the be-all-end-all either. This is due to the way some industries operate.

For example, in the oil and gas industry, many companies have cash flow positive operations. This means that they can sell their oil for more than the amount of money they spend on actually producing it (including paying employee salaries, and other general operational costs).

This is called having a positive Operating Cash Flow (OCF).

Some companies choose to pay out a dividend from this positive surplus of cash.

Other companies reinvest this surplus cash back into growing the company.

Oil and gas companies generally favor the latter, which includes drilling new wells and developing the rest of their projects in order to grow their production and revenue.

And these capital investments are not considered part of the Operating Cash Flow because they are not part of the company’s current operations. Because of this, many oil and gas companies have a positive OCF, but negative earnings.

How does a company have +OCF but have negative earnings?

For many businesses, an appropriate amount of leverage (debt) can help the company grow faster than it would otherwise. For this reason, the standard payout ratio calculated from a company’s net earnings is sometimes not the best indicator to use if the company is paying a regular dividend (but still prioritizing growth). In these cases, we can instead calculate a payout ratio based on the company’s OCF by comparing its dividend payout with its OCF, rather than its earnings.

In the chart below we once again use Exxon’s past performance as an example.

Note that the dividend to OCF ratio looks much healthier than the standard divided to earnings payout ratio. And you’ll notice there was still a spike around 2016 when global oil markets were depressed and revenues were down.

Looking at this chart, it’s not hard to conclude that Exxon is not in the same position of financial strength it was in before the oil price collapse of 2015-2016, and it still hasn’t recovered fully. I do not own Exxon.

Current State of the North American Dividend Market

As Raymond DeVoe Jr. once wisely stated…

“More money has been lost reaching for yield than at the point of a gun.”

Understanding resource cyclicality is absolutely critical to success in the resource sector. And that statement couldn’t be truer when it comes to resource stocks.

So what’s going on with the dividends of North American public companies?

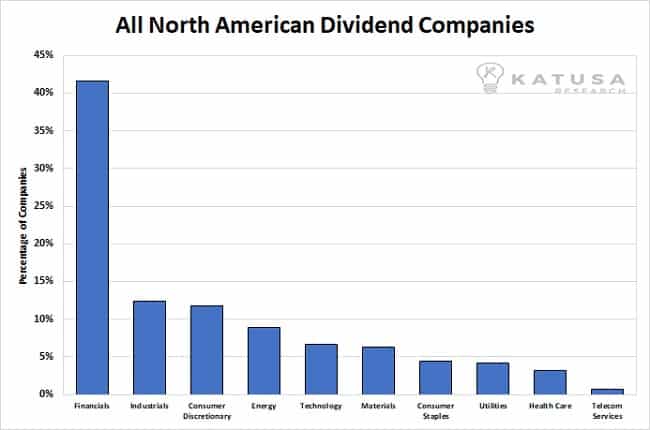

Below is a chart that shows the percentage of companies which pay a dividend in each sector.

There are over 2,000 companies that pay a dividend on the Canadian and U.S. stock exchanges today.

Banks, lenders, and other financial institutions such as investment trusts account for the largest portion as over 40% of these companies pay some form of dividend. They are followed by the industrial and consumer discretionary sectors. Less than 10% of the energy and mining companies pay a dividend.

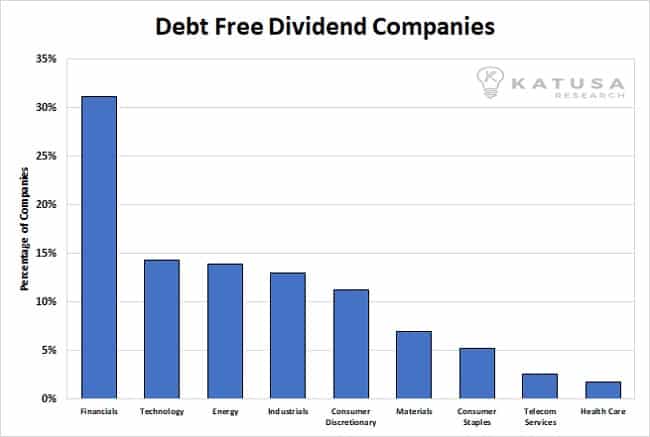

Of all these companies, only 231 (or just over 10%) are debt free companies. Below is a chart of the sector breakdown for the debt-free dividend-paying companies.

The mix here is quite similar to the overall dividend chart. However, certain sectors are better represented here than in the overall mix, such as the energy and tech industries.

So it’s a much more exclusive club, sure. But how exactly are these debt-free dividend companies better than the regular ones, you ask?

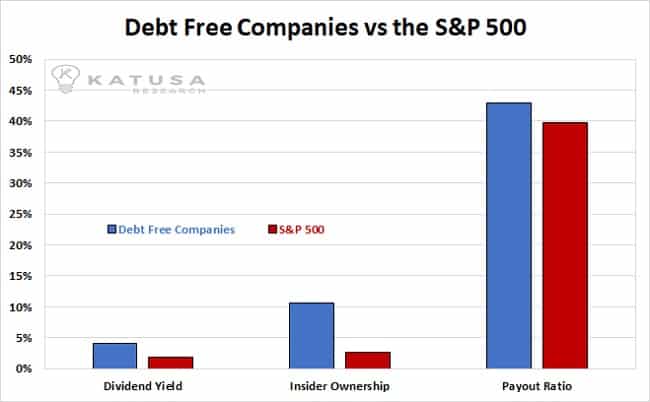

Below is a chart which shows the dividend yield, insider ownership, and payout ratio for debt-free companies versus the average in the S&P 500.

The chart above is a great chart that really confirms the whole “skin in the game” concept. The blue bars show that the better companies have a larger ownership by insiders. (Long-time readers know I love investing alongside management teams with lots of skin in the game).

Unsurprisingly, not only does management own more stock in the companies with less debt, but they also pay a better yield.

Additionally, the payout ratio is higher because there are no looming interest payments.

Drilling Deep for Dividends

Dividends in the resource sector are few and far between.

It is more common for a mining company to reinvest its cash flow back into exploration or advancing other projects rather than paying out capital. But when the mining companies do go the dividend route, the payouts can be better than the industry norm.

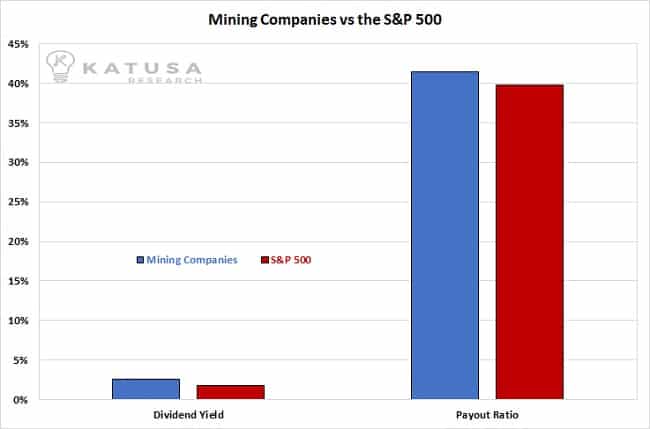

Below is a chart which shows the average dividend yield and payout ratios for mining companies versus the S&P 500.

As you can see, right now the dividends from the mining industry, on average, yield slightly better than the S&P 500. All this despite the fact that we’re currently in one of the weakest resource markets in recent memory.

And, as one would expect, the payout ratio for mining companies is slightly higher as well.

As a whole, the North American mining industry paid out USD $2.0 billion in dividends last year, while taking in some $13.7 billion in public funding through IPOs and private placements (from juniors to majors). This resulted in a “yield” of 15% for the industry in 2017.

W here am I Putting my Money?

There’s nothing like getting paid handsomely while waiting for your investment thesis to play out.

If you’re putting money into a company, a healthy (and big) dividend makes a company all the more attractive to have in your portfolio.

Where most investors fail is that they only chase yield. Just because a company is paying a 10% dividend, doesn’t mean it’s sustainable. If you see a sky-high dividend, you should immediately question the inputs. Is this sustainable?

But if you can find a company that can pay you a solid dividend and also has a colossal upside – then you’ve found a recipe for a major investment score. And I’ve found one such company and have big confidence in this dream team of management (I’m building a big position in this company).

Now going back to my intro…

On June 6th, 2018 I am going to publish, a new company recommendation that owns a project as impressive as Northern Dynasty’s Pebble, with the same massive upside potential as Pebble.

If you have followed my work, you know that those who followed my early recommendation on Pebble made over 1000% gains. I am not saying this company will go up 1000% the way Northern Dynasty did for us.

What I’m saying is this company has a Pebble-like upside that has the potential to deliver significant returns to shareholders – even in a notoriously stagnant resource equity market.

I’ll be finishing the due diligence by sometime next week. More details on this in my June issue.

Regards,

Marin

P.S. I believe I’m on to the best dividend stories in North America. And the dividend is just the tip of the iceberg… This company is going to be a game changer in the Western Hemisphere and disrupt an industry that very few people understand. I’m personally going to be betting very big on this company. To get all my research and analysis (and most importantly the name of this company and my buy-in tranche guidelines), consider becoming a subscriber to my research service, Katusa’s Resource Opportunities by clicking here.