How would you feel if you found out that the average American billionaire pays less in taxes than you do?

Not just a little less. In fact, one of them has paid zero taxes in ten of the last fifteen years. In 2016 and 2017, he paid $750 a year in income taxes.

That’s likely much less than you paid.

Of course… it’s U.S. President Donald Trump.

Here’s the thing: this is by no means uncommon in the United States.

Warren Buffett, the fourth richest man in the world, famously pays a lower tax rate than his secretary.

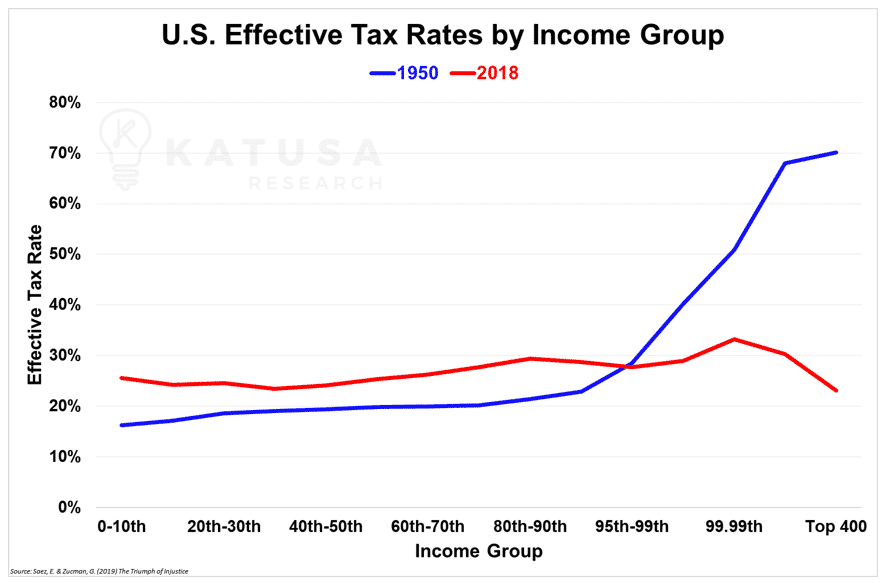

In 2018, the wealthiest 400 families in the United States paid an average tax rate of 23 percent. Meanwhile the bottom half of U.S. households paid… an average rate of 24.2 percent in income taxes.

You’re probably starting to figure it out by now: the system is rigged. And it isn’t in your favor.

Because this isn’t tax evasion. There’s nothing illegal about it. It’s perfectly legal tax avoidance.

And this is the way the game is meant to be played.

History has seen some oddball tax collections, including:

A tax on soap during the middle ages,

A beard tax in 1700’s Russia (this would work well on modern hipsters),

A tax on fireplaces in 1600’s England,

A tax on the numbers of windows on your house in 1696 England, and

A tax on hats in England.

Some taxes might be difficult to escape.

But if you’re ultra-wealthy, you can afford to pay a smart accountant to figure out how to not pay income taxes, legally.

If you’re not… pay up.

We got here from decades of the convoluted tax system being slowly bent in favor of high-income households.

Among the very percentile of earners, the average tax rate has dropped 50 percent in fifty years—from 51 percent to 26 percent.

This, despite a soaring federal deficit.

Governments are spending trillions to keep their economies and financial markets afloat.

The potential disaster of an underwhelming fiscal and monetary response is more concerning than a balanced budget or AAA credit rating in 2020.

With trillions of dollars’ worth of stimulus spending being deployed by governments all across the world, many might ask:

If the government can print all this money to cover obligations…

And create all this paper wealth out of thin air…

Then WHY do you still need to pay taxes?

You’d think that sooner or later, the government will catch on and get its fair share from the top income earners.

As it turns out, there’s a magic percentage at which high-income earners will both continue working and pay their taxes—meaning that’s where the government should theoretically set the upper tax bracket.

If a government set a 0% tax rate, they would obviously get no tax revenue. If they had a 100% tax rate, they’d also get no revenue… because nobody would work.

Between these two points is a curve that fluctuates as you adjust the tax rate. That curve is known as the “Laffer curve”, named after economist Arthur Laffer.

Which begs the question:

If the government doesn’t care about getting as much money as possible from the ultra-rich…

If the richest people in the U.S. are paying less in taxes every year…

If fewer people are paying taxes each year…

If the leader of the free world doesn’t even pay income taxes…

Why should the middle class have to pay taxes at all?

The Boomerang Money Act of 2020

The immediate, middle school answer is that taxes are necessary to pay for everything the government does.

For example, think back to six months ago, when Congress passed the CARES Act. It laid out an unprecedented $2.2 trillion in stimulus that was intended to help deal with the economic fallout from COVID-19.

(Just to put that amount in perspective, that amount of money was equal to India’s entire 2016 GDP. And India has a population of 1.4 billion people.)

It’s the closest we’ve seen to helicopter money in the United States. The only difference… is that helicopter money would be printed by the U.S. government and handed out.

The $1,200 stimulus check you probably received was paid for by your taxes.

The same money you sent the government last year is just being thrown back at you in the form of a check.

And there’s at least one more round of stimulus payments coming.

The CARES Act also implemented the Paycheck Protection Program. By the time the program ended, it was supporting 84 percent of small business employees in the U.S.

The PPP program was so generous that 25 percent of Americans who were out of the workforce made more than when they were working.

And that’s just the money you can actually see being spent.

The Federal Reserve has also provided another $3 trillion in liquidity to the capital markets so far, in addition to almost half a billion in SWAP Lines to its allies.

They’re now even loaning money directly to companies. The unprecedented, “unlimited” program buys high-quality bonds from huge companies, like Apple… and also junk bonds from unfavorable investments.

So maybe that’s the reason why you have to pay taxes. The Fed has to get all that money to make unlimited loans to unpromising companies from somewhere!

The Not-so-Federal Reserve

But that can’t be the case. Because right now, the Fed itself is spewing out new money faster than the machines can print.

Since February 2020, the Fed has increased the money supply by nearly as much as the entire money supply that existed in 2008 (adjusted for inflation).

The economic situation is so shaky in this crisis that no one can accurately forecast how much revenue will be lost from tax deferrals, shuttered businesses and unemployed households.

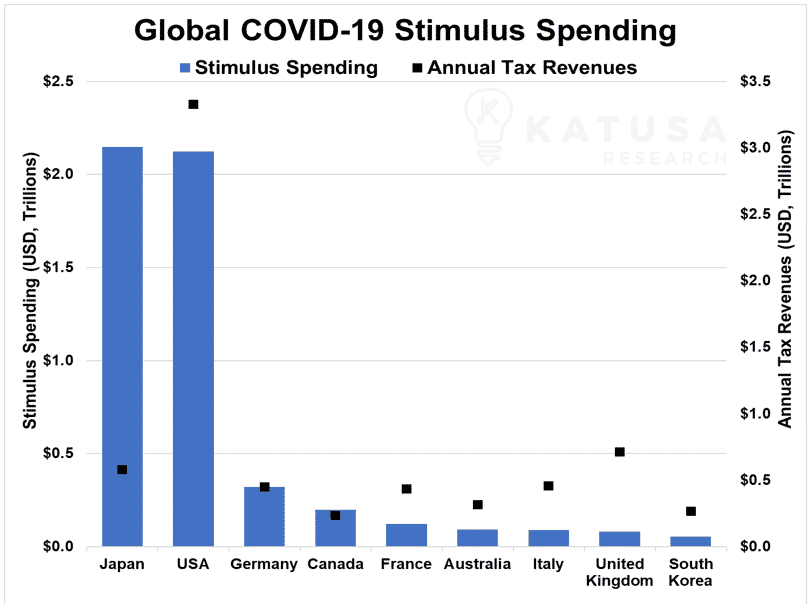

In the next chart, a plot of stimulus spending (blue bar) vs reported tax revenues (black dots), you can see that the amount the U.S. has committed to stimulus spending is over 85% of their 2019 tax revenue.

Total U.S. federal spending in 2019 amounted to nearly $4.5 trillion.

The amount of announced stimulus spending thus far represents an increase of 47% over last year’s budget.

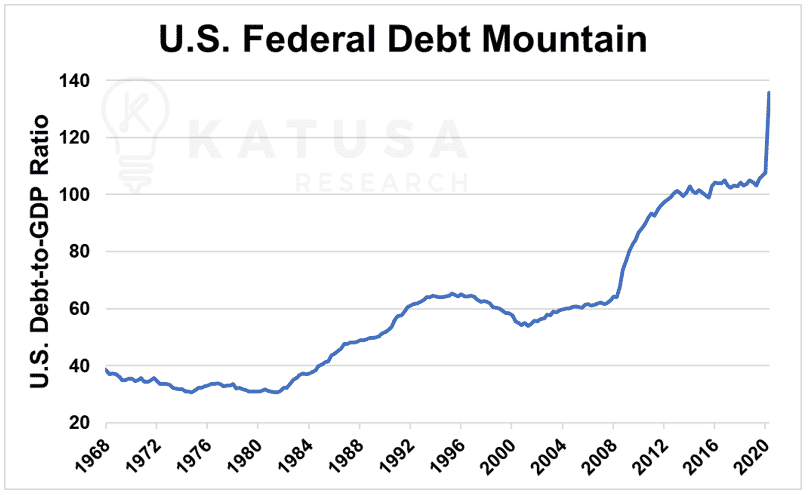

With the U.S. federal government already running fiscal deficits even in normal budgetary years (most recently to the tune of $984 billion), every dollar of revenue becomes increasingly more important.

The U.S. government debt situation has been in a serious mess ever since the 2008 Global Financial Crisis, when it jumped from around 60% to over 100% of GDP.

Think of GDP (Gross Domestic Product) as a proxy for the amount of taxable wealth generated within a country’s borders for a given period.

The U.S. is now well on its way to having a debt level that’s over 1.2x the amount of wealth created in the country each year.

Is This Sustainable?

Until the bond markets and ratings agencies say otherwise, the current levels of stimulus spending should be considered sustainable…

So long as the phrase “full faith and credit of the United States” continues to mean something.

But the reality is that a lot of economists and investors don’t want to imagine a scenario in which the U.S. Treasury defaults on its debt and the global economy collapses beyond repair.

This kind of risk never gets priced into any models.

Not because it’s too unlikely to occur or unpleasant to consider, but because it’s the kind of financial Doomsday scenario where you should be more worried about how you’re going to defend yourself from Mad Max-style raiders, than about asset prices.

No Money, No Limit

When Jerome Powell was asked how many dollars the Fed could print, he said: “There’s no limit.”

Where are all of those dollars going? Well, the U.S. Treasury is flooding the market with trillions of dollars in new debt, called Treasury notes (T-notes).

They’re like a credit card for the federal government.

Here’s how they work…

Investors buy a T-note, thereby lending money to the government. The government then owes the investor money, plus interest, due in a specific period of time.

It’s a nearly risk-free investment. After all, the U.S. has a AAA credit rating, and it’s not expected to default. And taxpayers can be counted on to pay taxes in time, which can be used to service the T-note debt.

Without taxes, few investors would want to buy T-notes. And the United States would quickly lose its ability to raise cheap money to pay its expenses.

Remember those dollars the Fed is printing, though? If the government ever “runs out” of money and can’t sell enough T-notes to investors, it can turn to… you guessed it… the Federal Reserve.

The Fed can print money, then send it to the Treasury Department to buy debt. Any interest paid out on the debt goes directly back to the Treasury.

That means the United States can spend as much money as it wants. It can always be financed by an entity that never has to care about money.

The Federal Reserve has a literal monopoly on money.

Hold on!

If the government can print as much money as it needs, and your own taxes are going toward stimulus payments to yourself…

Why not just pay less in taxes? Wouldn’t that stimulate the economy just as well—or more?

Or, for the multitrillion-dollar question—why do you and I pay taxes at all?

Inflation – A Tax by Any Other Name

Imagine that you never had to pay taxes again. Every year, you suddenly have an extra $20k–$50k to play around with.

Save it for retirement. Invest it. Pay for your kids’ tuition. Wouldn’t that be wonderful?

There’s a reason that’s a fairytale, and it’s quite simple: Paying taxes gives our money value.

Let me explain.

As citizens, we don’t actually need money. We need the goods that money buys.

So does the government. Imagine if the government printed all the money it needed to fund its own purchases of goods and services.

All of a sudden, more dollars—yours and the governments’—would be chasing the same amount of goods and services.

The dollars you earn would suddenly be worthless in comparison to what goods cost.

Whoever spent the money first would get the lowest price of goods. Once the new dollars were spent, prices would get pushed up. And they’d stay up, because those new dollars wouldn’t just disappear.

In other words, when the government prints money for itself to use, it’s still taxing you—only now it’s by bidding up the prices of the things your money can buy.

When the government prints money, you pay for it.

Put simply, taxation is a check on the U.S. government.

You did not vote for Jerome Powell. So inflation as a result of his monetary policy decisions amount to taxation without representation. Americans have held tea parties for less than that.

While inflation is hidden—you don’t see a byline for it on your paycheck—taxes are directly withdrawn from your bank account.

They have to take your money from you in broad daylight, circa April 15 every year.

Remember, though, how aggressively the Fed is increasing the money supply?

The taxation without representation—the midnight robbery of U.S. citizens at the gunpoint of inflation—is happening right now.

As prices start to rise, citizens will intuitively perceive the tax of inflation. And they’ll turn away from savings and push money into assets they believe will protect them.

And that’s when the real problems will begin.

Will You Be Locked Out of Paradise?

Not everyone is able to escape inflation.

People who can buy solid assets—gold, for example—will. Others will “short” the dollar by buying a mortgage or taking on debt.

Those who cannot will be over a barrel:

Young people taking on student loans will have no shelter from inflation. When they finally graduate, they’ll be unable to acquire assets.

People on a fixed income, such as Social Security recipients, will watch their checks simply evaporate.

Hard workers with retirement accounts will have to work even later in life just to have enough to finally retire.

Here’s the bottom line: while many citizens still pay taxes, all of this is already beginning to happen.

You’re telling your kids to save every penny. You’re paying your mortgage on time.

You’re doing everything you can to stay out of debt.

Meanwhile, the government is spending recklessly and printing money to cover for it.

Certain classes of society are receiving free handouts from the government faster than they can give them out.

The ultra-wealthy can finagle their way out of taxes or at least paying the same rate as you and I, and they can afford to find the best investment opportunities to make themselves even wealthier.

And you’re stuck smack-dab in the middle.

I say if you can’t beat them… join them.

Government Moral Hazard and Your Ticket Out

For the first time in history, the lines between fiscal and monetary policy are blurred, as finance ministries, banking institutions, legislatures, asset managers and central bankers all work in unison to combat COVID-19.

BlackRock, the world’s largest asset manager and ‘shadow bank’, has been tapped to manage the Fed’s corporate bond buying program – much to the chagrin of rival firms like State Street and Vanguard.

While stimulus spending is the foremost concern for taxpayers, everyone should be aware of the moral hazard that the Fed is creating from its trillion-dollar balance sheet expansion.

For regular investors, risky investments may offer higher returns, but the tradeoff is the potential to lose most, or perhaps all of your capital.

For BlackRock and the Fed’s bond buying program, however, that’s not a problem, because the government can simply print more money to replace what’s lost.

On top of that, it’s not even BlackRock’s money, and they’ll earn their fees either way.

With all this taken into account, one thing’s for certain – we’re in for some rough seas in the years to come.

Global economies and markets will power their way through the pandemic downturn, by hook or by crook.

The market is going to be volatile in the months and years ahead as the global pandemic downturn unwinds itself.

Volatility and uncertainty present investment opportunities—the kind that can make you wealthy enough to not have to pay taxes.

I started Katusa’s Resource Opportunities to make sure people like you have access to the best assets and opportunities to grow your wealth that money can buy. And that’s regardless of what stunt the Federal Reserve pulls next.

You can watch the value of your money fade away over the next few years. Or you can seize this opportunity to grow your wealth.

Legal Disclosure: By using this site, please assume Marin Katusa, Katusa Research and its employees have a financial interest in all companies and sectors mentioned on the website. The information provided is for informational purposes only and is not a recommendation to buy or sell any security. This is not financial advice.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

You can revoke your consent any time using the Revoke consent button.

Regards,

Regards,